Trading platform & site functionality

TokenHedg’s home page speaks the language of an institutional fund manager—“disciplined investment approach,” “competent risk‑adjusted returns,” and sector verticals that span private equity, real estate, infrastructure, insurance solutions, and renewable power. Yet what the site actually provides is a veneer: marketing sections, a login/signup portal, a chat widget, and a scattered crypto price chart widget. Nothing on the site resembles a regulated portal with required disclosures, legal documents, or detailed investment mandates. The design appears to rely on standard templates and front‑end libraries to produce a modern look without the substance a real manager would show.

Technically, the site loads familiar components (Bootstrap, jQuery, swiper carousels) and embeds a CryptoCompare chart. A live chat widget is injected, and, tellingly, the site pushes a WhatsApp contact path—unusual and inappropriate for a firm allegedly operating across heavily regulated financial verticals. We also observed a “calculator.js” reference and assets labeled like portfolios and testimonials, suggesting a marketing build rather than an audited investor portal. There is no evidence of a secure client area tied to a recognized custodian, transfer agent, or secure document vault for offering memoranda and investor reporting.

Navigation links imply a large institution—private equity, infrastructure, real estate, insurance, renewable power—but click‑throughs yield generic copy rather than detailed strategies, audited results, or investment committee bios. We did not find a fee schedule, performance track record, third‑party audit attestations, or custodian details. The absence of concrete operations behind a slick template is a classic signal of a shell site whose primary function is prospecting leads. When a site claims institutional scope but shows no institutional proof, treat it as a hazard zone rather than a due‑diligenced platform.

License & regulatory status

Legitimate asset managers and investment distributors who solicit funds from the public must display clear authorization in each jurisdiction where they market, such as FCA permissions in the UK, BaFin or CONSOB credentials in the EU, ASIC in Australia, and SEC/CFTC/FINRA registrations in the United States. TokenHedg provides none of this: there is no regulator name, no license number, no Form ADV link, and no MiFID passporting detail. Even boutique funds will name their legal entity, company number, registered office, administrator, and custodian. None of that is present here, which indicates either a complete disregard for regulation or an intent to avoid scrutiny.

Our review did not identify any regulatory filings or entries for TokenHedg in the public records we typically cross‑reference for managers, brokers, or promoters. That does not mean a regulator has published a formal warning yet—many fraudulent sites operate for months before enforcement notices appear—but the burden is on the operator to prove authorization, not on the public to assume it exists. Without verifiable oversight by a named authority (FCA, ASIC, BaFin, SEC, or similar), any claims of risk management and investor protection are marketing fiction.

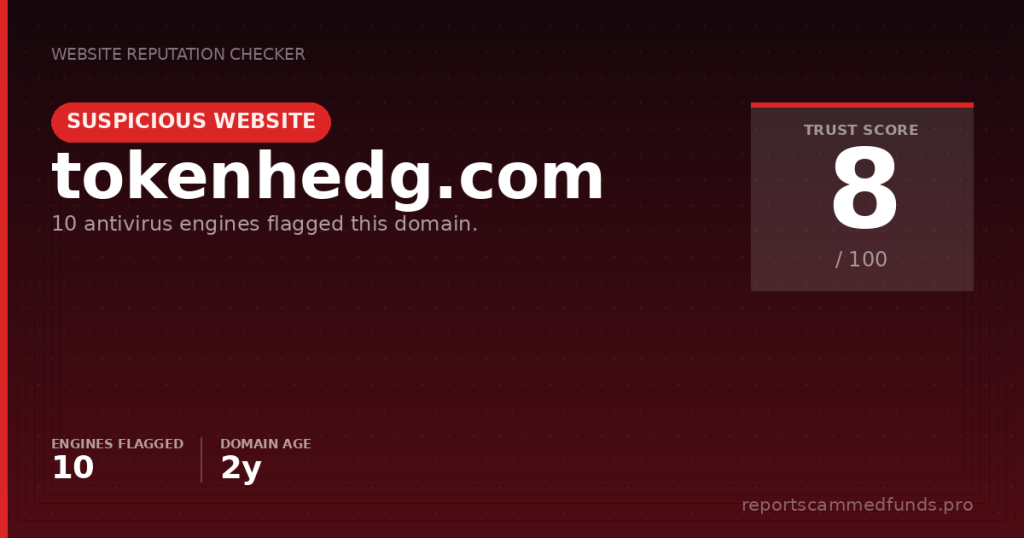

We also note that automated reputation checks show multiple security vendors flagging the domain as malicious or suspicious. This corroborates the regulatory gap and underscores how the site currently sits outside recognized supervisory frameworks. Taken together—no license data, no verifiable company identity, and safety flags—the regulatory profile is unacceptable for anyone considering a deposit or account creation.

User feedback

Because the domain is relatively new and lacks a public track record, we did not locate a body of credible, third‑party investor reviews or professional coverage that would substantiate TokenHedg’s claims. The absence of verified commentary is unsurprising for a low‑history, unlicensed site and should be treated as a warning, not a neutral data point. Authentic funds accumulate coverage—audits, filings, trustee notes, limited partner letters—over time; shell sites accumulate none.

From our broader casework, unregulated platforms that look and sound like TokenHedg often follow the same script. After a smooth onboarding conversation via chat or WhatsApp, deposits are requested with the promise of exceptional performance. When profits are shown on a dashboard, withdrawal attempts trigger “compliance” hurdles: surprise KYC after the fact, unexplained tax pre‑payments, or arbitrary “account upgrade” fees. These are telltale patterns of boiler‑room operations and advance‑fee fraud, not the behavior of transparent fiduciaries.

We also track a recurring tactic in which “account managers” or purported “experts” offer managed‑account trading and then rapidly generate losses while blaming market volatility. The investor, who cannot verify real trade execution, is pushed to deposit more to “average down” or unlock a “recovery plan.” Even if TokenHedg has not yet accrued public complaints, all the structural signals are consistent with operations that end in withdrawal blockages and vanishing support once funds are trapped.

Deposits & withdrawals

TokenHedg does not clearly disclose accepted funding methods, fee schedules, or withdrawal timelines on its public pages. That omission is, in itself, unacceptable for an entity marketing investments. Legitimate platforms state precisely how clients can fund (cards, bank wires, approved e‑money providers) and how redemptions are processed (cutoff times, settlement windows, possible charges, and anti‑money‑laundering checks). Here, the investor is simply funneled to a signup form and a chat/WhatsApp channel.

In the wild, setups like this commonly push investors to send funds by bank transfer or, increasingly, by crypto to third‑party wallets. Once money leaves the regulated banking perimeter—especially into crypto wallets under someone else’s control—recovery chances drop sharply. Without transparent custody or third‑party escrow, there is no neutral party overseeing where deposits land, how they are safeguarded, or when they can be returned.

Redemption friction is another hallmark. Unregulated sites routinely impose fabricated “compliance reviews,” phantom tax prepayments, or new verification conditions only after the investor clicks withdraw. These are pressure levers designed to extract more money or stall until the operator disappears. A legitimate manager discloses AML/KYC upfront, uses named custodians or fund administrators, and does not demand ad‑hoc payments to release your own capital or profits.

Why unregulated brokers are risky

Placing money with an unregulated website eliminates the safety rails that protect investors in supervised markets. There is no prudential oversight of client assets, no segregation from operating funds, and no obligation to keep your money at a named, tier‑one custodian. If the operator decides to freeze your account, impose invented fees, or delete the site, there is no binding regime forcing them to act fairly or return funds.

In regulated environments, you have recourse: you can complain to the firm’s compliance officer, escalate to the regulator, or pursue ombudsman schemes. You may also benefit from compensation schemes (e.g., FSCS in the UK) or SIPC‑style protections in securities contexts when assets are properly held. With TokenHedg, none of those protections are visible, and none are claimed with evidence. You are trusting an anonymous operator on the strength of a glossy template.

Beyond financial loss, there are data‑privacy risks. Submitting passports, licenses, and bank statements to an unknown entity hands criminals the keys to identity theft. Recovery scammers also trawl such sites, targeting victims with fake “chargeback” services that demand upfront fees and deliver nothing. The prudent approach is to avoid unregulated operators entirely and only deal with entities you can verify in official regulator registers.

How to get help if you’ve been scammed

If you already deposited money, act immediately. Contact your bank or card issuer to request a chargeback or recall; provide them with dates, amounts, recipient details, and screenshots of all communications. If you sent a wire, ask your bank’s fraud team to attempt a SWIFT recall and to flag the beneficiary account as suspected fraud. If you used a crypto exchange, open a ticket right away and ask for a freeze/trace on the destination wallet, then enable every security control (2FA, withdrawal locks) on your own account.

Report the incident to your national authorities. In the UK, file with Action Fraud; in the US, submit a complaint to the FBI’s IC3; in the EU, contact your local police and, where relevant, your national securities regulator (FCA, BaFin, CONSOB, or equivalent). Include the website (tokenhedg.com), the WhatsApp number if used, wallet addresses, and transaction hashes. Early reporting increases the odds that banks or exchanges can intervene before funds are fully laundered.

You do not need to face this alone. Our team at reportscammedfunds.pro reviews cases like this daily and can help you structure evidence, coordinate with your bank, and avoid secondary “recovery scam” traps. Reach out via reportscammedfunds.pro for a free triage assessment; we will outline realistic next steps, including dispute letters, law‑enforcement referrals, and ongoing monitoring. Do not pay anyone who cold‑contacts you promising guaranteed recovery—legitimate professionals do not demand upfront fees for unverifiable outcomes.

Conclusion

TokenHedg’s presentation as a multi‑asset, risk‑managed investment house is not backed by licenses, verified corporate details, or audited disclosures. The heavy use of templates, a WhatsApp sales funnel, and multiple safety flags from reputation checks are incompatible with a genuine regulated manager. When the core facts an investor needs are missing—who are you, where are the funds held, who regulates you—the only rational conclusion is to disengage.

We therefore recommend that readers do not sign up, do not deposit, and do not share identity documents with tokenhedg.com. If you are exploring investment opportunities, start from regulator registers and independent fund databases, not from cold contacts or glossy websites making expansive promises. Real firms are proud to cite their regulators, license numbers, administrators, and auditors; they do not hide them.

If you have been contacted by someone claiming to represent TokenHedg or pressuring you to act quickly, treat it as a boiler‑room approach and stop communication. Document everything, alert your bank, and consult professionals who will put your safety first. The safest profit is the one you never risked with an unverified, unregulated operator.