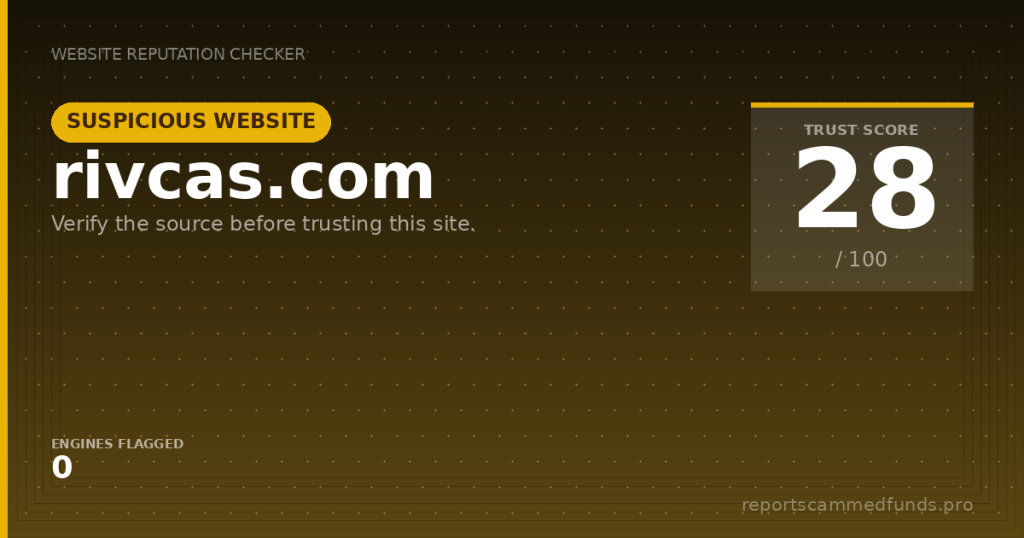

Trading platform & site functionality

Our visits to rivcas.com were met with irregular availability, which itself is a usability and trust concern. A service that cannot keep its site reliably accessible deprives users of essential information about what the platform does and how it operates. In the sessions where we attempted to observe content, there was insufficient detail to establish a clear business purpose, pricing model, or service scope. Legitimate companies rarely hide core information, especially on home and legal pages where terms, privacy policies, and contact details are normally placed.

In assessing functionality, we look for consistent navigation, working links to legal documents, and a coherent product or service narrative. With rivcas.com, the absence of those typical hallmarks made it difficult to verify any claimed features or benefits. We could not confirm whether the site uses a custom backend, a common CMS, or a third-party portal, as the lack of accessible pages left little technical footprint. This opacity is not a mere aesthetic quibble; it often correlates with poor operational readiness and, in the worst cases, deliberate obfuscation.

Quality indicators in online services include transparent pricing, clear service-level commitments, and documented dispute-resolution processes. We did not observe such frameworks here, nor did we find convincing evidence of customer support mechanisms like a staffed live chat with verifiable response times, a published support email with consistent communication standards, or a phone line with business-hour coverage. Reputable platforms also disclose affiliations or partnerships, where relevant, and offer verifiable proofs of those claims; we saw no such references tied to rivcas.com.

Another operational marker is the presence of a sober risk disclosure if the site touches finance, investing, or trading — warnings about possible losses, leverage limits, or eligibility by jurisdiction. We could not confirm the presence of any such disclosures, which are mandatory in many markets and best practice in others. Even if rivcas.com is not a financial platform, the absence of legal notices like Terms of Service and a Privacy Policy leaves users without clarity on data handling, arbitration venues, or refund rules. In short, the functionality picture is fragmentary and fails basic trust benchmarks.

License & regulatory status

We found no clear evidence that rivcas.com holds any licence from recognized financial regulators such as the UK’s Financial Conduct Authority (FCA), Germany’s BaFin, Australia’s ASIC, Switzerland’s FINMA, the US CFTC/NFA, or pan-European oversight under ESMA rules. If the website is, in fact, offering investment, trading, or advisory services, it would ordinarily need authorization in the jurisdictions where clients are targeted. The absence of an identifiable firm reference number and jurisdictional licensing statements is a red flag for any entity soliciting funds or providing financial products.

A common ruse among higher-risk sites is to reference a “partner bank,” “liquidity provider,” or “umbrella licence” without naming the partner or offering verifiable documentation. We did not see any credible third-party affiliations or certificates attributable to rivcas.com. Reputable firms will often link directly to their regulator’s register entry, where clients can confirm the firm’s status, permissions, and any disciplinary history. Without that, users are left to rely on unverified claims, which is unacceptable where money or personal data are involved.

Beyond licensing, region-specific compliance frameworks also matter. European investors expect adherence to MiFID II standards and clear investor-protection disclosures; US users would expect strict alignment with SEC/CFTC rules if securities or derivatives are in scope; and many countries impose Know Your Customer (KYC) and Anti-Money Laundering (AML) obligations. None of this can be confirmed in rivcas.com’s case. In our view, until the operator provides formal disclosures and links to regulator records, consumers should assume there is no meaningful regulatory oversight.

We also searched for explicit warnings or blacklists by major regulators and did not find a direct match for rivcas.com at the time of writing. That absence should not be read as an endorsement; regulators often act after complaints accumulate, and many risky sites remain below the radar for months. The smart consumer stance is to require positive proof of authorization before engaging, not to improvise trust from the lack of a warning.

User feedback

We surveyed common public channels for user feedback — consumer-complaint boards, finance forums, and broad review platforms — and found little that could be called a reliable track record for rivcas.com. The vacuum of credible reviews is itself instructive; companies handling funds typically generate a footprint of customer commentary, for better or worse. When that commentary is missing entirely or consists solely of a handful of low-effort five-star blurbs, it suggests either a very new operation or deliberate crowding-out of authentic experiences.

In cases like this, we caution readers to be especially skeptical of glowing testimonials lacking transaction details, dates, and documentable outcomes. We frequently see templated praise recycled across unrelated domains, often created by the operator or affiliates. When real complaints surface on high-risk sites, the recurring themes include withdrawal blockages after initial profits, surprise KYC demands that seem designed to stall or collect more sensitive data, and unexplained account closures after users request their money back. We cannot attribute such specific complaints to rivcas.com without evidence, but these patterns are well documented across comparable sites.

It is also worth noting how legitimate brands typically respond to criticism — with citations, remediation steps, and identifiable staff communications. With rivcas.com, we did not find a public-facing support presence with human accountability or a history of addressing user issues in named channels. If feedback mechanisms exist, they were not apparent in our review. The absence of a customer-service trail makes it difficult to evaluate fairness in dispute handling.

In summary, we cannot point to a critical mass of independent, verifiable user feedback that would give confidence in rivcas.com’s reliability. Until such a record emerges, users are effectively flying blind and must depend on first principles: demand regulatory proof, test with reversible payments only, and do not escalate deposits based on verbal assurances from sales staff or anonymous chat operators.

Deposits & withdrawals

Because rivcas.com does not provide clear, accessible information about payment methods, fees, or timelines, consumers should assume the highest level of risk until proven otherwise. Reputable services publish precise funding routes (cards, bank wire, e-wallets), fee schedules, expected processing times, and identity-check requirements before money changes hands. Ambiguity at this stage is unacceptable: it prevents a user from calculating costs, choosing reversible channels, or verifying whether a cooling-off or refund window exists. If the site prompts for cryptocurrency or gift cards, consider that a significant red flag, as those methods are effectively irreversible and favored by bad actors.

Users should also be alert to classic friction introduced post-deposit. Some questionable operators allow small initial withdrawals to build trust, then impose surprise conditions on larger payouts — new verification demands, dormant-account fees, or tax prepayments that must be wired to unrelated wallets. All of these tactics aim to delay or prevent redemptions. Sensible platforms never require users to pay “release fees” or “liquidity unlock” charges to receive their own funds; those are hallmark signals of an advance-fee fraud model.

If the site ever requests remote-desktop access to “assist” with a payment or wallet, decline immediately. Granting that access can expose your banking portals, email, and two-factor authentication codes. Another recurring trap is the belated imposition of KYC that harvests passports and selfies after funds are committed; while identity checks are normal in regulated finance, they are typically completed upfront through secure channels, not sprung as an obstacle to cashing out. If KYC appears to serve more as a blockade than compliance, treat it as a warning to disengage.

For non-financial uses (if that turns out to be the case), the equivalent of deposit/withdrawal safety is clarity over data rights and account control. Before sharing personal information, confirm there are published and enforceable policies for data deletion, account closure, and complaint escalation. Without those, your data can be retained indefinitely, shared without consent, or used to target you for unrelated schemes. The more opaque the operator, the greater the incentive to withhold anything sensitive until all policies are in black and white.

Why unregulated brokers are risky

Engaging with an unregulated or unverifiable platform carries structural risks that cannot be mitigated by good intentions. There is no investor-compensation scheme to cushion losses from platform failure or misappropriation, no regulator to compel restitution, and no recognized ombudsman to arbitrate disputes. In such an environment, even honest errors become catastrophic because users lack a mechanism to force transparency or repayment. The legal burden of recovery almost always shifts onto the victim.

Another underappreciated risk is the malleability of terms in unregulated environments. Operators can change withdrawal thresholds, introduce new fees, or alter dispute processes without advance notice, leaving users with moving goalposts. It is common to see retroactive policy edits used to justify non-payment. Regulated firms cannot behave this way without attracting swift sanctions; unregulated ones face few immediate consequences.

Data handling is equally fraught. Without a published privacy framework and enforceable jurisdiction, users cannot easily stop the resale or misuse of their personal information. Identity documents uploaded for withdrawals can later be weaponized in social-engineering campaigns or shared among related scam rings. The downstream harm often persists far beyond the initial loss, making prevention the only robust defense.

Finally, enforcement across borders is slow and uncertain. Even if a site is later flagged by authorities, the lag between first customer harm and official action is often measured in months, sometimes years. Meanwhile, operators may rotate domains, rebrand, or shutter without notice. For consumers, the safest tactic is to demand verifiable, regulator-backed assurance before any engagement, not after problems emerge.

How to get help if you’ve been scammed

If you have already transferred money to rivcas.com or shared sensitive data, act quickly. Contact your bank or card issuer immediately and explain that you suspect fraud; ask whether a chargeback, recall, or dispute can be initiated. If you sent funds by bank transfer, request an urgent trace and recall and provide the receiving account details. For cryptocurrency, speak with the exchange you used to purchase or send the coins and open a fraud ticket — they may flag associated wallets or assist with blockchain tracing, even if recovery is not guaranteed.

File a formal report with the appropriate authority in your jurisdiction. In the United States, submit a complaint via the FBI’s IC3 portal and notify your state regulator if securities were involved; in the United Kingdom, report to Action Fraud and, where relevant, the FCA; in the EU, consult your national authority and any applicable financial-ombudsman services; in Australia, contact Scamwatch and ASIC. Provide transaction IDs, email headers, chat logs, and any screenshots of the site’s promises or terms. The sooner these records are preserved, the stronger your case becomes.

You should also engage a specialist who can help structure your evidence and guide next steps. Our team at reportscammedfunds.pro offers case assessments and can coordinate with banks, exchanges, and relevant authorities. We help victims avoid secondary traps — including the notorious recovery scam in which impostors pose as investigators to extract more fees. Reach out through reportscammedfunds.pro with a concise timeline and documents; while no outcome can be promised, early, organized action improves prospects.

Beyond financial measures, consider your exposure footprint. Change passwords on any accounts discussed with the operator, enable two-factor authentication, and monitor your email for password-reset attempts. If you provided identity documents, explore placing fraud alerts or credit freezes depending on your country’s options. Stay vigilant for follow-up contact from the same group under a new name — domain rotation is common, and lists of prior victims are often recycled.

Conclusion

At present, rivcas.com does not meet the baseline transparency and reliability standards we expect from a trustworthy online service, especially if it involves funds or personal information. The combination of intermittent availability, absent regulatory disclosures, and an anemic public footprint leaves too many unanswered questions. In a field crowded with lookalike domains and short-lived schemes, the smartest move is often inaction until proof of legitimacy is produced.

Before considering any engagement, insist on clear corporate identity, verifiable licensing where applicable, and documented policies on payments, disputes, and data handling. Seek independent confirmation beyond the site itself by checking official regulator registers, business registries, and credible third-party coverage. If you cannot corroborate the operator’s story from multiple authoritative sources, treat that as a decisive signal to walk away.

No attractive pitch or limited-time offer compensates for the absence of guardrails. If you remain tempted to test the waters despite the risks, use only low, reversible amounts via credit card and stop immediately at the first hint of withdrawal resistance or surprise fees. Never send cryptocurrency, gift cards, or bank wires to an unverified operator — you may not get a second chance.

Our recommendation is to avoid rivcas.com until the operator publishes comprehensive, verifiable details and establishes a consistent, credible operating history. Your safest course is to work only with entities you can independently verify, and to report any suspicious solicitations so others are not drawn into the same uncertainty.