Trading platform & site functionality

OKX presents a broad crypto platform: spot markets, futures and options, a Web3 wallet, and staking/earn features. The front‑end is a polished, React‑based interface routing through a mix of Cloudflare and proprietary CDN assets. For charting and order entry, the interface is modern and fairly dense, with multiple tabs for different product lines and regional landing pages (including a United States–specific view). A captcha screen sometimes appears on first visit, which is common for high‑traffic exchanges defending against bots.

Beyond the exchange, OKX promotes a Web3 portal (web3.okx.com) tied to its wallet, enabling token swaps, DeFi access, and NFT interactions. This extension into Web3 widens the attack surface and the learning curve; while not a red flag, it means users should lock down 2FA, seed phrases, and device hygiene because a compromise in one component can cascade. The site also integrates cookie‑consent tooling and device fingerprinting (for fraud prevention and compliance), which tracks activity more closely than a basic informational site.

Coverage includes a deep lineup of crypto pairs and derivatives. Fees and funding rates can be competitive, but they fluctuate with volume tiers and product type, and they differ across regions. Users who prefer simple buy/sell may be routed to card processors or bank transfer providers that charge their own fees, while pros can access more granular fee schedules for maker/taker activity. The presence of a demo mode (paper trading) is a useful training wheel for new derivatives users.

One notable area is the P2P marketplace for fiat on/off‑ramp. It can be convenient where banking rails are fragile, but it also brings counterparty and chargeback risks that novice users can underestimate. Platform‑level security features (HSTS, TLS 1.3, captcha, session monitoring) appear robust, yet those protect only the perimeter; inside the account, choices like leverage, P2P counterparties, and bonus opt‑ins remain the user’s responsibility. In short, the tooling is feature‑rich and professional, but the complexity mandates caution.

License & regulatory status

Licensing for crypto venues is not uniform worldwide, and OKX’s public disclosures reflect that patchwork reality. The operator says it holds registrations or permissions in certain jurisdictions and blocks some geographies from specific products, but we did not see regulator licence numbers listed prominently on the core pages we reviewed, nor could we independently verify each claimed registration in real time. In markets like the UK, EU, UAE, and Australia, firms often need VASP registration or equivalent; in the United States, money transmitter rules, state‑by‑state permissions, and enforcement by the CFTC/SEC can limit derivatives access. Users should therefore cross‑check OKX’s stated permissions against local regulator registers (for example, FCA, BaFin, ASIC, VARA/ADGM, CONSOB, or ESMA‑linked databases) before funding.

We did not find current, formal public warnings from major regulators naming OKX as a fraud, but the absence of a warning is not the same as a blanket approval to operate all products in all places. Over the past two years, multiple jurisdictions tightened rules on marketing and promotions; exchanges have responded with geo‑specific subpages and disclaimers. If you reside in a tightly regulated market, confirm whether you are dealing with an entity appropriately registered for your area and whether leveraged products are allowed. If you cannot locate a clear local registration or if customer agreements reference offshore entities without local oversight, treat the relationship as higher risk and size your exposure accordingly.

User feedback

Public feedback about OKX is mixed, which is typical for large crypto venues. Supporters cite reliable uptime during regional trading hours, deep liquidity on major pairs, and competitive fees after volume discounts. They also highlight that order execution is fast, features keep pace with the industry, and the mobile apps are regularly updated. Advanced users appreciate the breadth of derivatives, options, and API connectivity.

On the other hand, aggregated review sites and forums include frequent frustration about compliance holds and verification escalations that trigger after funds have been deposited or after profitable trading. Themes include withdrawal blockages “pending review,” requests for additional documents or source‑of‑funds letters, and slow resolution timelines when support queues are backed up. P2P disputes appear as a recurring pain point, where buyers or sellers disagree on payment confirmations; while OKX provides an escrow process, outcomes may still feel opaque to users unfamiliar with the rules. A smaller but notable set of posts mention surprise KYC steps to unlock fiat channels that were not obvious at signup.

There are also periodic complaints related to derivatives liquidations—especially from traders who used high leverage or misunderstood funding mechanics. This isn’t unique to OKX; any futures venue with cross‑margin or isolated margin can result in fast losses if risk settings are mishandled. However, the educational burden still sits with the user, and negative reviews tend to surface after emotionally charged events. The pattern to take away is not that the platform is a scam, but that complexity and compliance can combine to produce hard stops that feel punitive if you are not prepared.

Deposits & withdrawals

OKX supports crypto deposits and withdrawals across many networks, which are typically processed quickly once on‑chain confirmations settle. For fiat, availability depends heavily on the user’s country: some regions have bank transfers, card purchases via third‑party processors, or a P2P marketplace where users match with merchants. Each method carries distinct fees—network fees for crypto, processor spreads for cards, and potential escrow or exchange‑rate costs for P2P. Users should confirm exact fees within their account and read the terms of any third‑party payment integration.

Withdrawals are where friction most often appears. Large or unusual transactions can trigger Know‑Your‑Customer/Anti‑Money‑Laundering reviews, source‑of‑funds checks, or sanctions screening, which may pause withdrawals until documents are provided and reviewed. This is not uncommon in the sector and is not, on its own, evidence of wrongdoing; still, you should plan for it. Keep high‑resolution scans of your ID and banking documents ready, and never rely on time‑sensitive obligations (like a property closing) being met by same‑day exchange withdrawals.

If you use the P2P marketplace for fiat on/off‑ramp, document every step: screenshots of chats, bank transfer receipts, and merchant profiles. Never release crypto before independently confirming receipt in your bank account, and beware of chargebacks from reversible payment methods. In dispute cases, escalate through the platform’s provided tools quickly and respond with detailed evidence. For large sums, professional OTC channels or fully regulated local rails are often safer, even if fees look slightly higher up front.

Why unregulated brokers are risky

With crypto venues, the phrase “unregulated” rarely means entirely lawless; it usually signals that some products or entities operate without the same investor‑protection framework you expect from a licensed securities broker. That has consequences: no deposit insurance, limited recourse if an offshore entity fails, and a heavier burden on you to read terms, margin rules, and dispute processes. Even when an exchange is partially registered (for example, as a VASP) in certain regions, those permissions may not cover derivatives or marketing to your location. Practically, this means you should diversify where you keep funds, minimize idle balances on any single platform, and start with test withdrawals to validate that your account settings, KYC status, and regional rails behave as expected.

How to get help if you’ve been scammed

If you have already lost money or your withdrawal is frozen, act methodically. First, contact OKX support via your account and request a clear explanation of any compliance review, then provide only the documents requested through official channels—never via unsolicited links or DMs. If your loss involved a card or bank transfer to a third‑party processor or a P2P merchant and you suspect fraud, immediately contact your issuing bank to ask about a chargeback or a recall; speed matters. File a report with your national authority (for example, Action Fraud in the UK, IC3.gov in the US, your country’s financial crimes unit, or the relevant securities/commodities regulator like the FCA, BaFin, ASIC, or the CFTC). Finally, if you need structured assistance or forensic guidance on next steps, reach out to our team at reportscammedfunds.pro—we can review your documentation, help you triage options, and coordinate with your bank and the appropriate regulator.

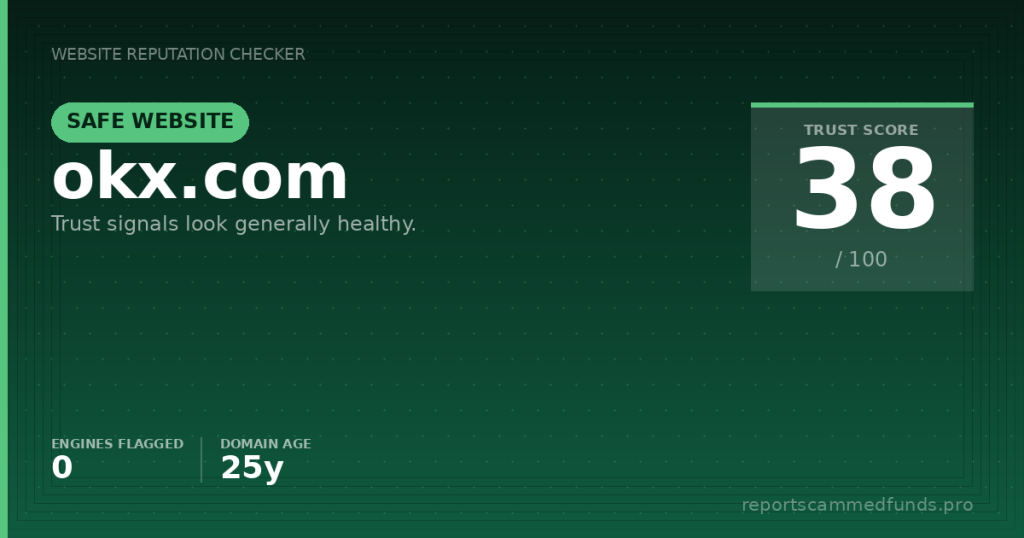

Conclusion

Our take is cautiously positive: okx.com is a long‑established, widely used exchange with no malware or phishing flags in our automated checks and a mature, professional platform. That said, the lived experience depends on your region, product choice, and documentation readiness; compliance holds and P2P disputes are real possibilities. If you choose to use OKX, verify that the specific entity serving you has the right permissions for your country and the product you intend to use, start with small test transfers, lock down 2FA and withdrawal whitelists, and keep meticulous records. This is not an outright scam, but it is also not a bank—treat it with the level of caution that complex, high‑speed financial software warrants.