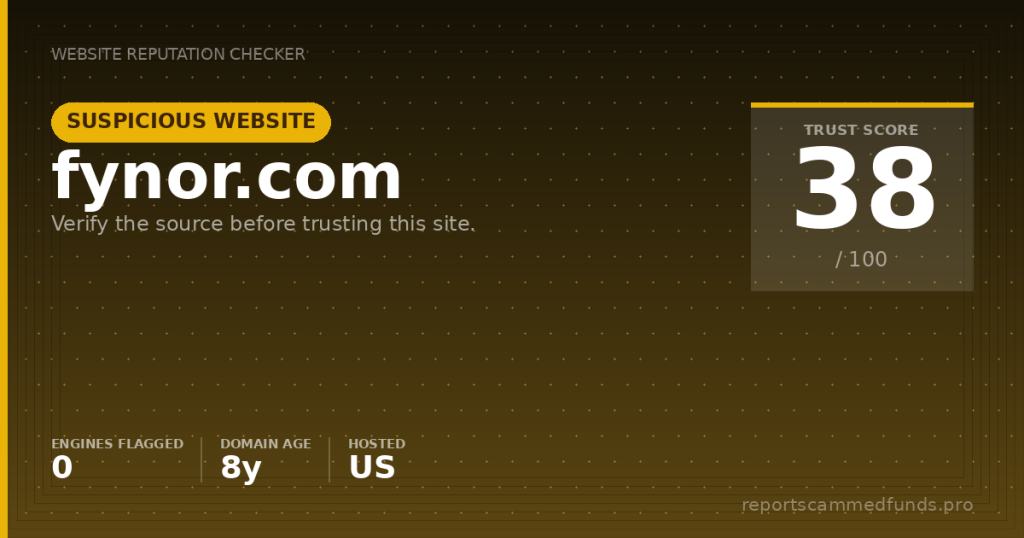

Trading platform & site functionality

FYNOR’s public pages market a one-stop crypto venue: buy and sell Bitcoin and altcoins, trade futures, stake tokens for passive earnings, and even interact with NFTs. The site redirects to an English-language path and presents a modern, app-like interface with a prominent registration flow. Navigation is polished and suggests a proprietary web platform rather than a white-label MetaTrader skin. From a casual inspection, the site loads over HTTPS and renders promptly, with standard elements like help widgets and social media icons. On the surface, the experience looks contemporary and on par with newer exchanges.

Beyond the marketing veneer, the operational details that matter to traders are less transparent. We could not easily locate a precise maker/taker fee grid, financing rates for perpetuals, or a published schedule of withdrawal costs without account creation. Likewise, there was no clear, public order-book depth snapshot or historical uptime page, both of which help assess liquidity and reliability. The platform claims spot and futures coverage along with staking, but the exact list of supported networks, NFT standards, and margin parameters is not obvious from the landing pages. That lack of granular, pre-login detail makes it harder to evaluate FYNOR against established, transparent competitors.

As with many web-first crypto venues, FYNOR appears to rely on a browser-based interface, possibly supplemented by mobile apps, although we did not see independently verifiable download links or store listings during review. There are no references to third-party trading platforms like MT4/MT5, which suggests any derivatives are executed through FYNOR’s own stack. Proprietary stacks can be fine, but they also mean you depend entirely on the operator’s handling of outages, order routing, and liquidation logic. Without independent benchmarks or SOC reports, prospective users have to take a leap of faith on execution quality. That is a meaningful decision when leverage and volatile assets are involved.

We did note standard web hygiene signals such as a valid TLS certificate and a locale-based redirect, both of which are routine but expected for a platform that claims to serve global traffic. However, the absence of easily found legal documents beyond generic terms, and the lack of a clearly named corporate owner, leave unanswered questions about who holds client funds and under what legal regime. The site’s presentation is competent, and the domain has been around for years, but presentation alone is not a substitute for verifiable safeguards. Before opening an account, a prudent user would need to see a full fee schedule, proof of reserves or equivalent attestations, and clear statements about custody and regulatory oversight. Those fundamentals are not obvious from FYNOR’s public pages.

License & regulatory status

In most major jurisdictions, a platform that facilitates crypto spot trading must satisfy anti-money-laundering registration rules at a minimum, and a platform that offers futures or other derivatives typically needs explicit authorisation. In the United Kingdom, cryptoasset exchange providers must be registered for AML supervision with the FCA, and derivatives offered to retail face additional restrictions. Across the European Union, MiCA brings a harmonised framework with licensing and consumer-protection obligations for crypto-asset service providers. In the United States, money transmission triggers state-by-state licensing and federal registration as an MSB, while derivatives fall under the CFTC’s remit for designated contract markets and futures commission merchants. Australia, Canada, and other G20 countries enforce similar regimes via AUSTRAC, provincial securities commissions, and equivalent regulators.

Against that backdrop, we looked for regulator references, licence numbers, or a named legal entity on the FYNOR site that could be checked in public registries. None were apparent on the pages we reviewed, and no licence numbers were disclosed alongside the futures and staking claims. We did not encounter any official warnings from major regulators about FYNOR while compiling this report, but absence of a warning is not an endorsement and can simply mean the platform is operating below radar. The lack of public licensing information places responsibility entirely on the user to assess counterparty risk. Until FYNOR names a supervising authority and a corporate entity with a verifiable registration, it is reasonable to treat it as unregulated.

Derivatives in particular are a regulatory tripwire. Many regulators restrict or prohibit certain crypto derivatives from being marketed to retail clients, or they require the platform to apply appropriateness tests, leverage caps, and robust risk warnings. If FYNOR truly offers futures to users in multiple countries, it would normally need to implement geofencing and jurisdiction-specific compliance controls. We did not see clear indicators of such segmentation or a region-specific risk summary on the public site. That gap does not prove non-compliance, but it underscores how little the average consumer can verify before sending funds.

From a consumer-protection standpoint, regulation matters because it provides avenues for redress and standards for safeguarding client assets. Licensed platforms must operate within defined rules on capital, custody, disclosures, and marketing, and they are accountable to a named authority. Unregulated venues can function without these constraints, but that freedom transfers risk to the user: funds can be frozen without explanation, fees can be changed overnight, and disputes may be governed by opaque offshore terms. If FYNOR wishes to be taken seriously by risk-aware traders, publishing the legal entity, jurisdiction, and applicable regulatory permissions would be an important start. Without that, users should moderate their risk exposure accordingly.

User feedback

Public, independently verifiable feedback about FYNOR is sparse. The domain has been around for years, and the site presents polished marketing, but we did not find a large body of detailed user reviews on widely tracked consumer platforms. Social media links may point to active channels, although we did not independently verify the authenticity or moderation practices of those accounts. The quiet footprint could mean a small, niche operation or simply a newer push under an older domain. Either way, the absence of robust third-party commentary makes it difficult to assess real-world execution quality or customer service responsiveness.

When crypto platforms go wrong, the complaint patterns are often familiar. The most common themes include withdrawal blockages after profitable trades, surprise KYC escalations only after deposits or gains, and changing margin rules that trigger liquidations. We have not independently confirmed such issues on FYNOR, but the risk exists with any unregulated platform, and buyers should be alert for these red flags. Users should also watch for aggressive sales outreach, unsolicited investment advice, or requests to install remote-control software. Those tactics correlate with boiler-room operations and managed-account traps, which can lead to catastrophic losses.

Another recurring theme in consumer complaints across the sector is fee opacity. Traders sometimes discover marked-up network fees, withdrawal minimums that are far higher than expected, or “maintenance” charges introduced after the fact. When a platform lacks a clear, public fee page and versioned change logs, the probability of fee-related disputes increases. Again, we did not verify whether FYNOR engages in such practices, but the lack of easy-access information raises the risk profile. Transparent platforms tend to spotlight their fees because they know cost-sensitive traders will compare.

Customer support is often the tie-breaker in borderline cases. A live chat bubble and a contact form can be useful, but they are not substitutes for a well-defined escalation pathway with service-level commitments. If support takes days to respond, or if answers are scripted and fail to address a specific account issue, users quickly find themselves with funds in limbo. This is where regulatory oversight and a named corporate entity matter: they create accountability mechanisms outside of the platform’s own discretion. With FYNOR, the lack of a visible corporate identity and the limited public footprint add weight to the need for caution.

Deposits & withdrawals

Based on the site’s positioning, deposits and withdrawals likely support multiple cryptocurrencies, possibly alongside card or bank funding routes via partners. Without a publicly posted funding page, it is not clear which fiat channels, if any, are supported, or what the onboarding requirements are. Crypto funding is final once confirmations land, so users should test the smallest possible amount before entrusting meaningful capital to any platform. If the platform requires KYC, verify exactly when that kicks in and what documents are needed, so you do not face a surprise verification block when you try to withdraw. Absent clarity, assume that fiat options are limited and that crypto rails are the primary path.

Withdrawals are the single most important test of a platform’s integrity. Typical friction points include extended “processing times,” sudden requests for enhanced due diligence after profits, and vague references to compliance reviews that drag on for weeks. Reputable venues publish expected timelines per asset, explain the difference between internal processing and network confirmation times, and provide ticket-based escalation. If FYNOR cannot provide clear withdrawal ETAs and a transparent fee breakdown before you deposit, that should weigh heavily in your risk calculus. Always document every step of a withdrawal attempt, including screenshots and transaction IDs.

Fees are another area that deserves close scrutiny. Crypto withdrawals have on-chain network fees, but some platforms layer on administrative charges or set minimums that effectively lock small balances. For derivatives, there may be funding payments, liquidation fees, and overnight financing costs, all of which can erode returns. We did not see a detailed fee schedule on FYNOR’s public pages, which makes it hard to compare its economics against more established exchanges. If you cannot get a clear, stable fee table in writing, consider that a sign to limit your exposure.

Terms tied to bonuses, promotions, or staking returns can come back to haunt withdrawals. Across the industry, we have seen platforms cite “bonus turnover requirements,” “security holds,” or “insufficient staking epochs” as reasons to block or delay cash-outs. Before accepting any incentive, insist on the full terms and ensure you understand how they interact with your ability to withdraw principal and profits. If the language is ambiguous or gives the platform wide discretion, decline the incentive. Your ability to exit should never be contingent on fine print you cannot independently verify.

Why unregulated brokers are risky

Using an unregulated or unclearly regulated trading platform means you are not protected by investor-compensation schemes or prudential oversight. If the platform suffers a hack, freezes accounts, or becomes insolvent, there may be no authority to compel restitution. Complaints turn into contract disputes governed by the operator’s chosen jurisdiction, which could be offshore and difficult to litigate. Even if you win a judgment, collecting is another matter. That is why licensing and clear legal domiciles matter: they make accountability real rather than theoretical.

Custody is another overlooked risk. When you deposit crypto to a centralized platform, you do not control the private keys—effectively, you have an IOU from the operator. Without audited proof-of-reserves, segregated accounts, or third-party attestation, you must trust the platform’s internal accounting and risk management. History shows that trust can be misplaced, particularly when leverage and staking programs create implicit liabilities. The mantra “not your keys, not your coins” remains relevant, especially on platforms with opaque governance.

Marketing around staking and passive income can lull users into underestimating risk. Yields are a function of protocol risk, validator performance, and sometimes additional layers of rehypothecation or market making. If a platform is vague about how it sources yields or how it handles slashing and downtime, the promised returns may mask considerable downside. Staking programs can also have lock-up periods or epoch-dependency that frustrate withdrawals. Without concrete, audited disclosures, treat any yield narrative as promotional, not as a guarantee.

Finally, cross-border complexity compounds the problem. If a platform serves users in multiple countries without region-specific terms or licensing, the legal environment becomes murky. Disputes can fall into jurisdictional gaps, and regulators may disclaim authority if the operator lacks a local presence. Consumers end up relying on the platform’s goodwill or on the blunt instrument of public complaints. For risk-aware readers, that is a strong argument to keep balances minimal or to use venues with clear, enforceable oversight.

How to get help if you’ve been scammed

If you have already sent money and suspect a problem, act quickly. For card deposits, contact your card issuer immediately and request a chargeback under the appropriate reason code (for example, services not provided or misrepresentation). For bank wires, ask your bank to initiate a recall or a fraud report—time is critical, and outcomes vary by jurisdiction. Document every interaction with the platform: account statements, chat transcripts, emails, and screenshots of the dashboards. A clear paper trail strengthens your case with banks, regulators, and any investigators.

For crypto transfers, move to containment. Notify the platform where you originated the funds (if different) and ask them to flag the receiving address; some exchanges will place a compliance hold if subsequent inflows appear. If you can see on-chain movement, record the transaction hashes and any subsequent hops to known exchange deposit wallets. Consider filing a police report to obtain a case number; some crypto businesses will only engage substantively once law enforcement is involved. Do not pay anyone who approaches you with a “guaranteed recovery” pitch—recovery scams are common and often compound losses.

Report the incident to relevant authorities. In the United States, file with the FBI’s IC3 portal and notify your state regulator; in the United Kingdom, file with Action Fraud and inform the FCA if a crypto service has engaged you; in the EU, contact your national financial supervisor or police cybercrime unit; in Australia, report to Scamwatch and AUSTRAC if applicable. Provide copies of payment records and any representations the platform made to you. If derivatives or staking were involved, include the promotional materials and terms tied to those products. Regulator attention can help even when the platform is offshore, particularly if multiple victims come forward.

You can also reach our team at reportscammedfunds.pro for guidance on next steps, documentation prep, and liaison with banks and exchanges. We cannot guarantee outcomes, but we can help you frame a chargeback, draft regulator submissions, and avoid the many pitfalls that lead to dead ends. If you are still deciding whether to deposit, we can also help you run a pre-deposit due-diligence checklist. Whether you engage us or not, keep your expectations realistic and protect yourself from “no-win fee” recovery pitches that demand upfront payment. The earlier you seek qualified assistance, the better your odds.

Conclusion

FYNOR’s domain age, polished front end, and working HTTPS suggest a real operation rather than a throwaway scheme. However, the absence of disclosed regulatory licensing, the lack of a clearly named corporate entity, and the marketing of futures and staking without visible guardrails are significant concerns. That combination places the platform in the high-risk category, even if we have not verified specific consumer harm. Where money and leverage are involved, opacity is itself a material risk. Caution should be your default stance.

We do not label FYNOR a confirmed scam. We do, however, flag it as a venue that has not yet earned trust through transparency and verifiable oversight. If you decide to try it, limit exposure to amounts you can afford to lose, test withdrawals early with trivial sums, and avoid promotions that encumber your right to exit. Keep meticulous records and be prepared to cut losses if standard service assurances are not promptly met. The worst outcomes often follow a pattern of ignoring early warning signs.

Ultimately, many safer alternatives exist: platforms that publish their legal entity, list regulator permissions, and provide detailed, versioned fee pages and proof-of-reserves attestations. Until FYNOR meets that bar, it remains a speculative counterparty. Our recommendation is to withhold significant funds, demand written disclosures, and verify independently rather than relying on marketing claims. If you are already entangled, follow the remediation steps above and contact reportscammedfunds.pro for tailored assistance. Your best defense is disciplined due diligence before any deposit.