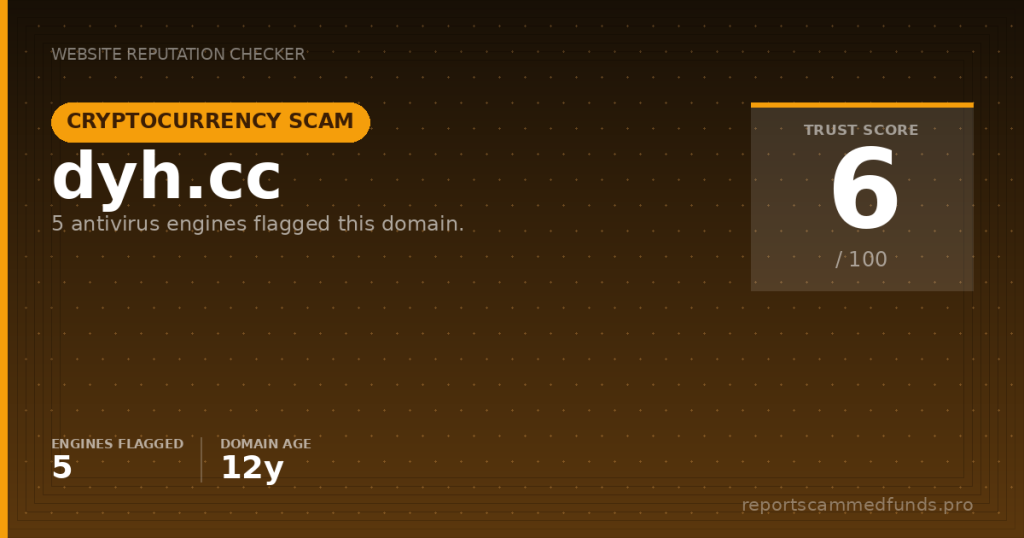

Trading platform & site functionality

On first load, dyh.cc redirects to a login-style page at a nested path, offering a minimal interface without transparent navigation to an About, Legal, or Contact section. The layout pulls in common front-end libraries (Bootstrap, jQuery, and Zepto) and presents the look of a generic web portal rather than a recognizable brand storefront. A prominent third-party live-chat widget initializes and begins logging usage events, suggesting the operator expects prospective users to engage privately before sharing details. Absent from the landing flow are crucial assurances: there is no published company name, no corporate address, and no visible compliance page that would normally earn user trust.

From a functional standpoint, the site behaves as a walled garden. Without an account, you cannot review fees, order types, supported assets, or the actual feature set. The prevalence of generic assets—static images, CSS, and a common JavaScript alert layer—indicates the shell of an application rather than a fully transparent trading venue. We did not see any public-facing status page, system health updates, or third-party performance telemetry that sophisticated platforms tend to publish to reassure new clients.

The heavy reliance on an external chat solution is telling. While live chat can be legitimate, in high-risk corners of the internet it is often used to shepherd prospects into manual payment flows or off-platform instructions, bypassing normal controls that leave evidence. There is no visible KYC/AML explainer, no link to withdrawal policies, no disclosure about safekeeping of client digital assets, and no indication of whether the site uses segregated accounts or insured custody. These omissions matter, especially for crypto—the sector with the fastest-growing roster of loss reports tied to unlicensed operators.

Technically, the site uses HTTPS with modern TLS and advertises HSTS, which is positive for transport security. But security of the connection does not equal trust in the operator. We found no sign of incident reporting, bug bounty, or SOC 2/ISO 27001 claims, and the cookie practices around session handling are not paired with a visible Privacy Policy. In other words, even if the page loads cleanly and looks polished, the trust scaffolding that should surround a financial venue is missing.

License & regulatory status

Any platform that takes custody of client funds—especially in crypto—should be prepared to show clear regulatory status. We looked for a license number, regulator name, or jurisdictional declarations across the landing experience and found none. There is no banner for FCA authorization in the UK, no reference to BaFin in Germany, no ASIC or AUSTRAC acknowledgment in Australia, and no North American registration footprints like FinCEN MSB or money-transmission licensing at the state level. The absence of licensing assertions is striking for a service that appears to solicit value-bearing interactions.

To contextualize, reputable crypto brokerages and exchanges typically provide direct links to their regulator entries, complete legal names, and corporate entity numbers. They also publish robust terms and risk disclosures, including information on leverage, margin requirements, and conflict-of-interest policies if applicable. On dyh.cc, we observed none of these elements in public view. If the operator is regulated, they are not showing it, which undermines confidence in their compliance posture.

We also checked for signals that might indicate false-affiliation claims—logos of major regulators, mentions of umbrella authorization, or vague statements like “licensed globally.” Those tactics are common among boiler-room style sites, but we did not see explicit name-dropping here. Instead, the problem is opacity: no company name, no address, and no licensing claims whatsoever. That may be less brazen than a fabricated license, but it is just as troubling for an investor seeking recourse and legal clarity.

It’s important to underline that not all crypto services require the same licenses in every country, but any platform seeking deposits should at minimum disclose who they are, what law governs the contract, and which authority—if any—oversees customer complaints. Where such basics are missing, users often find themselves outside the safety nets that regulators like the FCA, BaFin, ASIC, CONSOB, or the CFTC coordinate. Until the operator behind dyh.cc publishes verifiable corporate and supervisory details, we must treat it as an unregulated venue.

User feedback

We looked for credible, independently verifiable user reviews tied specifically to dyh.cc and did not find a meaningful body of feedback. That does not prove the site is new or that no one has used it, but it does mean there is no public track record to weigh. Established platforms usually accumulate forum threads, Trustpilot entries, social-media discussions, and technical support footprints that help prospective clients assess reliability. The near-silence here makes it harder to judge service quality and heightens the need for caution.

In the absence of verifiable testimonials, we pay more attention to structural risk markers: hidden content behind login, limited disclosures, and a reliance on private chat channels. In countless cases we’ve documented, these conditions precede common complaint patterns: surprise KYC requests only after users try to withdraw, fees invented on the spot to unlock funds, or “tax” demands that must be paid in cryptocurrency before releasing balances. We cannot say dyh.cc exhibits these behaviors, but the profile overlaps substantially with sites that do.

When complaints do surface for operations of this type, they often mention withdrawal blockages after profit, long delays with no support updates, or pressure to deposit more to “qualify” for payouts. Managed-account offers sometimes appear midstream, with representatives pushing users into higher-risk trades that quickly erase balances. Again, we are not alleging specific misconduct by dyh.cc; rather, we are outlining the risk spectrum historically associated with opaque, unlicensed, crypto-leaning portals so readers can make an informed decision.

Deposits & withdrawals

Because dyh.cc does not show funding details before account creation, users cannot review deposit channels or withdrawal processes without handing over personal data first. That’s a reversal of good practice: reputable firms let you review fee schedules, method availability (cards, bank wire, faster payments, SEPA, ACH), and any crypto wallet requirements up front. A transparent operator also provides timelines for withdrawals, minimum and maximum thresholds, and compliance checkpoints so there are no midstream surprises.

In many high-risk operations, cryptocurrency is heavily favored as a deposit method because it is fast and—crucially for scammers—harder to reverse than card payments. Users who proceed anyway should be extremely careful: send a tiny test amount first, demand written confirmation of fees and timelines, and never agree to pay an additional “release fee” or “tax” in crypto to unlock a withdrawal. If a platform will only accept crypto and refuses to process chargeback-eligible card transactions, that is a major warning sign.

The same scrutiny applies to withdrawals. If a representative introduces new KYC hurdles only after you request a payout, or if they require a fresh deposit to “verify the wallet,” stop and reassess. Genuine KYC is required before trading or at first deposit, not selectively at the withdrawal stage to stall or extract more money. Until dyh.cc publishes a clear, accessible funding and withdrawal policy with verifiable company details, users should assume there may be friction or outright refusal at the payout stage.

Why unregulated brokers are risky

Using an unregulated platform means you are operating outside the safety rails most investors rely on. There is no investor-compensation scheme to soften the blow of insolvency or misconduct, no supervisory body to receive your complaint, and no mandated segregation of client funds from company money. In practice, that often leaves customers with no practical recourse if the operator ceases communication or invents fees to block withdrawals.

Crypto heightens the stakes. Transfers can be irreversible, and offshore entities can vanish or morph domains quickly, leaving behind little more than a login page that no longer authenticates. Without regulator oversight, crucial internal processes—auditing, dispute resolution, custody controls—are matters of trust rather than enforceable standards. That asymmetry favors the operator at every step, not the customer.

For all these reasons, the threshold for proof must be higher. Before you send a cent, demand transparent ownership details, regulator links that resolve to current records, and written policies that you can save offline. If the operator cannot provide those basics—or requests crypto payments without alternatives—you are assuming an outsized, unrewarded risk.

How to get help if you’ve been scammed

If you already sent money to dyh.cc and are facing delays, fee demands, or a blocked withdrawal, act promptly. For card or bank payments, contact your bank immediately, explain the circumstances, and request a chargeback or recall where available. Document every interaction with the site: emails, chat transcripts, transaction IDs, and screenshots, as these may be essential for disputes and reporting.

Report the incident to your national authority. In the UK, submit to Action Fraud; in the US, file with the FTC and the FBI’s IC3; in the EU, notify your national regulator or police and consider alerts to ESMA-linked channels; in Australia, report to ASIC and Scamwatch. If any crypto was involved, contact your exchange’s compliance team at once to flag addresses and explore tracing or freezing options before funds are mixed or bridged away.

You can also request case assistance from our team at reportscammedfunds.pro. We help victims evaluate recovery avenues, prioritize chargeback windows, and avoid common secondary traps like “recovery scams” that demand up-front fees. Reach out via reportscammedfunds.pro with a timeline of events and available proof; we will review and advise on practical next steps tailored to your jurisdiction and payment rails.

Conclusion

Taken together—the absence of licensing, the lack of corporate transparency, the login-only content, and multiple security engines flagging risk—make dyh.cc a platform to avoid. While we cannot say definitively who operates it or what happens beyond the login, trustworthy venues do not ask you to leap blindfolded into funding. The burden of proof is on the operator, and so far, they are not meeting it.

If you are still considering engagement, insist on verifiable documents: legal entity name, address, regulator, and a clear client agreement you can keep. Test with a micro-deposit only after those basics are provided and confirmed, and never agree to off-platform payment instructions in private chat. Any pushback on these reasonable requests should be treated as a decisive red flag.

Our recommendation is to look elsewhere for crypto or trading services that publish their licenses, list their directors, and maintain transparent funding and withdrawal terms. Even then, perform your own checks and start small. Your best defense against financial harm is disciplined due diligence and skepticism toward operators that ask for trust without offering proof.