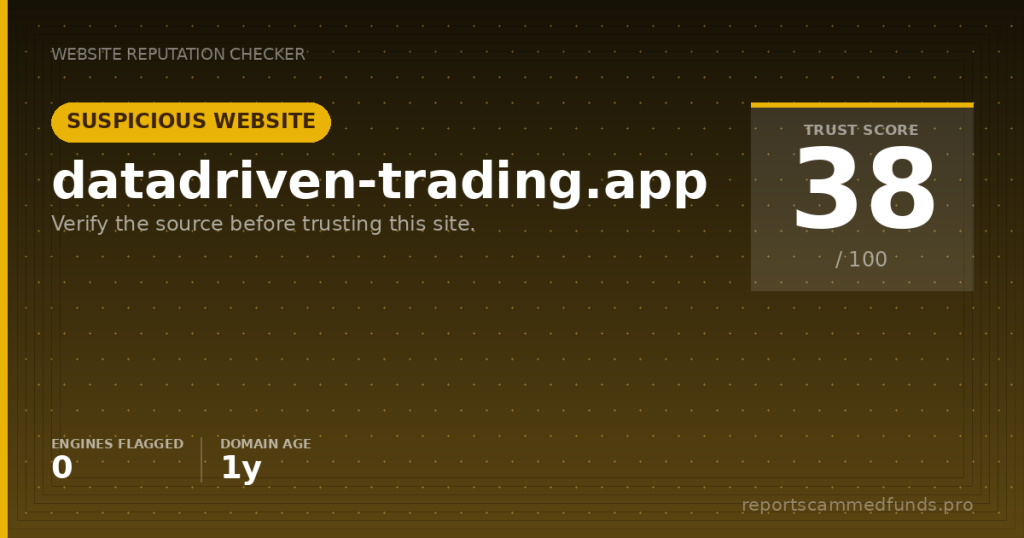

Trading platform & site functionality

Datadriven-trading.app loads as a polished promotional landing page for a trading brand called DataDriven Trading. The page renders a background marketing video through a YouTube iframe and uses static asset delivery for images via a content delivery network. The primary call to action launches an embedded Whop checkout in an iframe, indicating the product is likely a subscription or membership, rather than a brokerage account. In our browser capture, we saw the script reporting that both desktop and mobile video iframes loaded successfully, underscoring the emphasis on marketing content.

From a technical perspective, the site sits on modern cloud infrastructure, presents a valid TLS certificate, and returns assets consistently; there were no broken elements in our test load. It also references a manifest file, suggesting a lightweight app-style approach. However, functionality beyond the public landing page appears gated behind payment. There are no on-page details about the precise nature of the tools (for example, whether it’s an alert service, an indicator suite, or an education package), nor are there transparent performance metrics, risk disclosures, or a pricing table prior to invoking the third-party checkout.

Importantly, the site does not appear to be a broker; it does not offer order execution, trading accounts, or leverage. That means there is no native discussion of spreads, fees, or slippage—issues that apply to brokers rather than to tool vendors. Instead, the key quality concerns revolve around clarity: what exactly is included in the membership, how results are measured and shared, and what recourse a user has if the service disappoints. Those basics, which reputable research and education firms typically disclose up front, were not clearly laid out on the landing page we saw.

License & regulatory status

We did not find any licensing claims on datadriven-trading.app. Because the site is not a broker—no accounts, no leverage, no execution—it would not fall under direct brokerage regulation like FCA authorization in the UK or a CFTC/NFA membership in the US. That said, vendors that provide paid trading signals, performance claims, or personalized investment advice may fall under investment adviser regimes in some jurisdictions. In those cases, an absence of registration can be problematic if the service goes beyond general education and ventures into individualized advice for compensation.

In our review window, we did not see public warnings from major regulators such as FCA (UK), BaFin (Germany), ASIC (Australia), CONSOB (Italy), or the CFTC/SEC (US) that specifically name this domain. Absence of a warning is not an endorsement; most small or new operations simply haven’t drawn regulator attention yet. What matters for consumers is the presence of verifiable corporate details and clear, compliant disclaimers that define the product as education or tools only, not advice or guaranteed results. We could not independently verify such disclosures on the visible landing experience.

If the operator claims associations with licensed entities, third-party audits, or verified track records elsewhere (in social media or private conversations), insist on public, independently confirmable documentation. Authentic license numbers, where applicable, can be checked on regulator registers like the FCA Register, ASIC connect, or the Investment Adviser Public Disclosure system in the US. Any reluctance to furnish hard, checkable facts—or any claim that regulation is ‘not needed’ while simultaneously promising specific returns—should be treated as a pronounced red flag.

User feedback

We did not locate a body of independent, third‑party user reviews on mainstream platforms that would let us reliably gauge DataDriven Trading’s customer satisfaction. That may be a simple function of age: newly launched services often lack reviews until they accumulate real users. It can also arise when sales happen through closed ecosystems—here, purchase runs via an embedded Whop checkout—which may centralize feedback inside private communities and make it harder for outsiders to evaluate.

Because verifiable feedback is thin, prospective buyers should treat anecdotal testimonials on the brand’s own media channels with caution. In the trading space, common complaint themes include ‘withdrawal blockages after profit’ for brokers, and for tools/services: ‘unexpected upsells to managed accounts,’ ‘no-refund policies after login,’ ‘surprise KYC after payment,’ or ‘performance different from promoted screenshots.’ The latter points are especially relevant for a membership or indicator vendor where results are difficult to independently replicate without comprehensive logs and time-stamped signals.

If you come across social media promotions tied to this brand, check whether promoters disclose compensation or affiliate status. Boiler-room style pitches and hype-laden posts can be a sign of an aggressive marketing funnel rather than a stable, research‑led product. Conversely, absence of credible, critical review coverage elsewhere on the web should not be interpreted as a clean bill of health; it simply means you must generate your own due diligence—by asking for trial access, reading written policies closely, and confirming the operator’s business identity.

Deposits & withdrawals

This site does not accept deposits for trading, nor does it appear to custody client funds. Instead, a third‑party checkout on whop.com handles payment for a plan labeled in the embedded link. Payment methods on platforms like that typically include cards and sometimes digital wallets; cryptocurrency acceptance varies by seller. Because the transaction occurs through an external gateway, refund and cancellation rules may be dictated by the seller’s Whop storefront and the platform’s own terms, not by the landing page you are currently viewing.

Before you pay, scrutinize the checkout page for pricing cadence (monthly or annual auto‑renew), free-trial conditions, and any ‘no refunds after access’ clauses. Membership marketplaces can host both rigorous and casual vendors; in the latter case, policies may be minimal and refunds discretionary. It’s reasonable to request a sample deliverable (for example, anonymized past alerts, a dated track record with methodology, or a product demo) before committing. If you cannot get clarity in writing, assume that cancellation and refunds may be slow, tightly limited, or declined.

If you do purchase, prefer a payment method that preserves your rights—major credit cards generally allow chargebacks for nondelivery or misrepresentation. Avoid paying by irreversible means such as crypto unless you have already tested the service and fully trust the operator; chargebacks on blockchain transactions are not possible. Keep copies of the invoice, checkout page, terms visible at purchase, and any correspondence about cancellation—these documents are crucial if you later need to dispute a charge.

Why unregulated brokers are risky

Unregulated trading services pose a different risk profile from unlicensed brokers, but the core problem is similar: there is no investor‑protection framework to lean on if the service underperforms or vanishes. When you buy signals or tools from an opaque operator, you rely entirely on their integrity to honor refunds, maintain access, and present accurate performance. Consumer-protection avenues exist through your card issuer and local regulators, but those are after-the-fact remedies—not upfront safeguards.

Risk is magnified when marketing emphasizes effortless profits, offers only curated screenshots, or provides no method to verify results independently. Services that hard‑pivot from ‘tools’ to ‘managed accounts’ or introduce you to an offshore broker with high leverage often trigger a cascade of familiar scams: advance-fee traps, managed-account losses, and sudden KYC demands after you ask for a refund. While we did not observe those behaviors on datadriven-trading.app itself, the lack of explicit boundaries on the landing page means you should watch for them during any sales conversation.

Finally, remember that even sincere tool vendors can be wrong. Markets change, strategies decay, and the out-of-sample period is what matters. If you cannot validate a method with clear, time-stamped data and explanation, you are effectively buying a black box. Keep your position sizes trivial until you are confident the service adds value, and never let a vendor talk you into depositing with a ‘partner broker’ as a condition of membership—that’s a hallmark of higher-risk schemes.

How to get help if you’ve been scammed

If you already paid and something feels off—unresponsive support, denied refunds despite stated policies, or pressure to move money to a third-party broker—act promptly. First, contact your bank or card issuer and explain the facts; ask whether a chargeback is possible for nondelivery, misrepresentation, or an unauthorized recurring charge. Provide screenshots of the checkout, terms at the time of purchase, and any correspondence. Speed matters with card disputes, so don’t wait to see if things ‘work out.’

Second, make a formal report to the appropriate authority in your country. In the UK, use Action Fraud; in the US, file at IC3.gov for internet crime and notify your state securities regulator if advice may have been given. In the EU, consult your national consumer protection body and, if investment services were implied, your financial regulator (for example, BaFin in Germany, CONSOB in Italy). Regulators need your reports to spot patterns and to issue warnings that can help others.

Finally, if you need guidance assembling a case or want a second opinion on your options, our investigative team can help. Visit reportscammedfunds.pro to request assistance with documentation, escalation strategy, and outreach. We can review your evidence pack, identify the best route for recovery, and warn you about common secondary scams such as ‘recovery agents’ that demand upfront fees without delivering results. Contact us even if you are still in the evaluation stage; early input often prevents losses.

Conclusion

Datadriven-trading.app presents a slick, modern landing page and uses a recognizable third‑party checkout, which are positive signs compared to the boilerplate sites we often see in trading scams. At the same time, the operator’s identity is not plainly stated, there is no obvious audit trail for performance claims, and there is no regulatory oversight because the product is framed as tools or membership rather than brokerage. That combination does not convict the brand of wrongdoing, but it absolutely warrants slow, evidence‑led due diligence.

If you’re considering a purchase, ask for specifics in writing: who runs the company, where it is based, what’s included for the fee, how cancellations work, and how performance is calculated and verified. Request a sample or a limited trial, and pay only by a method that preserves your dispute rights. Decline any invitation to deposit at a ‘partner broker’ or to hand over remote access for a ‘managed account’—those are unrelated to a tool or education product and raise the risk profile substantially.

Our safety‑first recommendation is to pause and verify before you buy. If you cannot get straight answers or find independent, balanced reviews, treat that opacity as a cost you do not need to bear. Better options exist in the market: firms that state who they are, document their methods, and let you test before committing to recurring fees. If you proceed, size your risk accordingly and keep meticulous records.