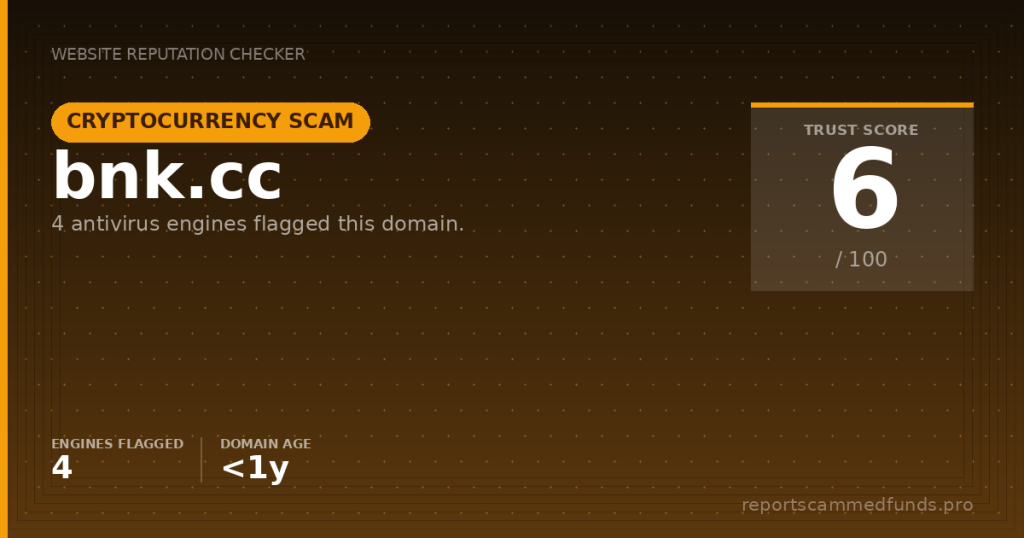

Trading platform & site functionality

BNK’s interface loads as a login-driven portal and immediately redirects from the root path to an index page, where users are met with a minimal, mobile-leaning layout that uses common front-end libraries. We observed references to Bootstrap, Zepto, and jQuery, alongside WeUI-style components, which signal a lightweight web portal rather than a well-documented trading platform. The site leverages an external chat widget and localized assets indicating multi-language support, yet it does not present a public ‘About’ page or a transparent service overview. This arrangement is consistent with private dashboards and gated portals, but it is also a hallmark of high-risk sites that conceal crucial disclosures behind a registration wall. The effect is that a prospective user must create an account to discover even basic information about fees, custody, and transaction policies.

Functionally, the site appears to target users interested in cryptocurrency activities, though it never explicitly sets out its business model in clear language. There is no publicly visible trading screen, product catalog, or pricing reference that would allow a neutral assessment of spreads, liquidity, or platform reliability. Instead, the visitor journey is driven by the chat module and a visual language toggle, leaving material questions unanswered: What assets are supported, who provides execution or custody, and how are funds segregated? In our testing, the portal remained mostly an interface stub without substantive documentation or trust scaffolding, such as audited financial statements or third-party attestations. In short, what is presented is primarily the sign-in shell of a platform rather than an operationally transparent service.

A closer look at the request logs shows frequent calls to a third-party messaging framework, likely used to initialize a sales or support drip. Chat-driven funnels are not inherently problematic, yet on a site with no public legal pages and no licensing disclosures, they create a risky dynamic that steers users toward registration and potential deposits before the facts are laid out. We also noted the absence of easily accessible terms and conditions, privacy disclosures, complaint handling policies, or explicit risk warnings on the visible pages. Even if such documents exist behind the login, best practice for financial services is to make core disclosures freely viewable. On balance, the functional design choices raise more questions than they answer.

License & regulatory status

We found no explicit licensing claims or regulator references on the pages we could access without an account. For financial services, especially those touching crypto exchange, brokerage, or custody, it is standard to provide regulator names and license identifiers on the public site. The absence of such detail on bnk.cc is significant. We cross-checked public registers for major jurisdictions—such as the FCA (UK), BaFin (Germany), ASIC (Australia), CONSOB (Italy), FINMA (Switzerland), and the CFTC/NFA (US)—and did not locate a clearly matching entry for this domain or an associated legal name; this could not be independently verified beyond the time of our review.

It is possible that the operator is offshore or claims a status that does not require licensing in a particular jurisdiction. However, that ambiguity still places consumers at a disadvantage, because dispute resolution and law enforcement reach depend heavily on where a firm is domiciled and licensed. In EU and UK contexts, retail-facing cryptoasset services typically require registration or approval to conduct certain activities, with anti-money laundering supervision at minimum. If a site cannot demonstrate such approvals or lists no legal entity at all, you are left with little recourse if funds are withheld or if the service disappears.

We also looked for third-party trust marks, audit seals, or any formal affiliations with recognized compliance bodies. None were visible on the public pages. Without a named company, license number, or jurisdictional anchor, claims of compliance cannot be evaluated. In our view, the regulatory picture is either absent or intentionally obscured, both of which are incompatible with safe investing.

User feedback

At the time of writing, we did not identify credible, independently verifiable customer reviews specific to bnk.cc that would allow for a balanced consumer-sentiment assessment. That lack of organic feedback is not uncommon for very young domains, but in the investment and crypto arena it is a cautionary sign—trusted platforms typically accumulate forum posts, third-party reviews, and social media threads that can be cross-checked. We advise readers to be wary of testimonials presented through the site’s own support channels or pop-up chats, which can be curated.

The broader pattern among similar login-gated crypto sites is consistent: users report ‘withdrawal blockages after profit,’ ‘surprise KYC only after deposit,’ escalating ‘verification fees’ that must be paid to unlock balances, and ‘managed-account schemes’ where a handler executes trades leading to sudden losses. While we cannot attribute these behaviors to bnk.cc without direct evidence, the platform presentation—limited public information, aggressive chat prompting, and no visible licensing—matches the conditions in which those complaints generally arise. A prudent approach is to assume you will face friction getting money back unless clear, pre-deposit withdrawal terms and legal contacts are published.

If you come across informal comments or private messages encouraging you to sign up via chat or messaging apps, consider that a boiler-room tactic rather than legitimate customer support. Investment-grade firms do not cold-message prospects on Telegram, WhatsApp, or site chats insisting on urgent deposits, bonuses, or matching offers. If such pressure tactics appear around this brand, treat them as a red flag and disengage.

Deposits & withdrawals

The site does not disclose, on its public-facing pages, what deposit methods it accepts or what the withdrawal process entails. That opacity matters. Card-accepting, regulated platforms normally present payment logos, a fee schedule, and step-by-step withdrawal guidance that can be read before registration. Here, the user is pushed to create an account and interact through a chat funnel without first seeing how funds can be reclaimed or how long withdrawals take.

In high-risk crypto schemes with similar layouts, deposits typically flow through irreversible rails like USDT, BTC, or other tokens on fast chains. Once sent, these transactions cannot be reversed, and recovering them requires exchange cooperation and sometimes chain-analytics triage. Poorly documented withdrawal pages, or those that suddenly demand extra ‘taxes,’ ‘gas fees,’ or ‘anti-money-laundering holds’ paid in crypto to release funds, are a hallmark of advance-fee fraud in the crypto-investment niche. Again, we cannot assert that bnk.cc uses these tactics—but the lack of published withdrawal terms keeps the door open for such practices.

Before committing any money, insist on seeing—and saving—formal withdrawal policies, fee tables, and identity/verification requirements, preferably in a downloadable format. Confirm whether the operator holds client funds in segregated accounts, whether there are daily/weekly caps, how failed withdrawals are escalated, and how disputes are handled. If the only path to answers is through a chat widget that resists providing written, official terms, that is not an acceptable substitute for transparent documentation.

Why unregulated brokers are risky

Using an unregulated or unverified platform places you outside the safety net of investor-protection regimes and ombudsman services. If something goes wrong—unexpected account freezes, ‘compliance’ demands for additional payments, disappeared balances, or outright non-response—you have no formal path to compel performance or restitution. Contrast that with regulated venues where regulators such as the FCA, ASIC, BaFin, or the CFTC can be notified, and where firms have legally binding complaint procedures.

There is also the privacy and data-security component. Sites that solicit identity documents without being under supervision present a double exposure: the funds at risk and the identity details that can be misused. If a platform cannot show how it complies with data-protection law, where servers are located, or who the data controller is, you should not upload passports, driver’s licenses, or proof-of-address documents.

Finally, unregulated players can vanish—domains expire, dashboards go dark, chats stop responding. Without a firm name, registered office, or public directors, there is little for your bank, law enforcement, or courts to latch onto. Prevention beats cure here: verify licensing before a single dollar leaves your control.

How to get help if you’ve been scammed

If you have already deposited with bnk.cc and face delays or denial of withdrawals, take action quickly. First, contact your bank or card issuer to request a chargeback or dispute if you used cards; provide a clear timeline, screenshots, and any written promises made by the platform. For crypto transfers, immediately alert the exchange or wallet provider you used to fund the deposit, submit a fraud report, and ask for transaction tagging; rapid exchange notifications can sometimes help prevent onward cash-outs.

Report the incident to your national authority. In the UK, use Action Fraud; in the US, file with the FBI’s IC3 and your state regulator; in the EU, notify your country’s financial regulator or police cybercrime unit. These reports create a paper trail and can be critical for any later recovery efforts. Keep copies of all chats, emails, transaction hashes, and KYC requests—organized evidence raises the odds of meaningful help.

Our publication supports victims with triage, documentation, and escalation. Visit reportscammedfunds.pro to request assistance on your case. We can help you structure your evidence, advise on chargeback narratives, interface with exchanges where appropriate, and flag recovery-scam approaches that often target recent victims. Do not pay ‘unlock fees’ or ‘tax prepayments’ demanded by the same platform or by supposed recovery agents—those are almost always part of the fraud cycle.

Conclusion

Given the very young domain age, multiple security-flag categorizations, and a total absence of publicly verifiable licensing or company identity, bnk.cc does not meet basic criteria for a trustworthy financial service. The heavy reliance on a chat widget to shepherd users into registration, without transparent terms and policies on the public site, further undermines confidence. This is not how reputable crypto or investment firms present themselves.

Until independently verifiable details are produced—legal entity name, jurisdiction, regulatory authorization, full fee and withdrawal schedules—our recommendation is to avoid depositing funds or sharing personal documents. If the operator can substantiate compliance, publish auditable policies, and address the risk findings flagged by reputation engines, this assessment can be revisited. For now, the burden of proof rests squarely with the site.

If you are considering this platform because of a persuasive message, referral, or ‘too good to be true’ returns, step back and verify. Consult official regulator registers, search for independent reviews, and compare against established, licensed alternatives. Your capital—and your identity—deserve better protection than a login screen and a sales chat can provide.