Trading platform & site functionality

CMTrading’s site positions the brand as a multi‑asset CFD brokerage serving retail traders with a focus on accessibility and education. The marketing emphasizes uncomplicated onboarding, with the familiar prompt to open a demo or live account and start trading quickly. Educational materials, webinars, and trading tips are often highlighted, which can be helpful for first‑time traders but also serve to funnel users toward activation and funding. The overall message is that trading is approachable and that the platform provides a guided path from beginner materials to live risk, a narrative common among retail CFD providers.

On platforms, CMTrading advertises MetaTrader 4 (MT4) alongside a browser‑based WebTrader interface, covering most of the basic charting and order‑execution needs for a retail audience. References to social or copy‑trading features, often branded under proprietary names, suggest that clients can mirror strategies of other traders. Copy trading is especially appealing to newcomers, but it can also mask leveraged risk and lead to unmanaged exposure if one becomes reliant on unknown signal providers. The platform proposition appears to revolve around ease of use, fast execution, and the ability to trade forex, indices, commodities, shares, and potentially some crypto CFDs, though not all of these can be independently verified from primary documents at the time of writing.

CMTrading’s account tiers resemble the standard Bronze/Silver/Gold/VIP segmentation seen across the sector, where higher deposits purportedly unlock tighter spreads, educational sessions, or faster support. While tiering can align service levels with client size, it can also incentivize larger deposits before a client has validated execution quality or withdrawal reliability. Spread and fee disclosures, when presented as ‘from’ rates, may not reflect typical trading conditions during volatile periods, and retail traders often discover wider effective costs than the headline suggests. As with any CFD broker, the fine print in the Terms and Conditions and product schedule matters more than glossy marketing pages.

Educational hubs and regular webinars are promoted as a differentiator, giving the impression of a coached experience. Done right, education is positive; done poorly, it becomes a funnel for overtrading or unjustified confidence. We caution readers to separate platform literacy (how to place and manage orders) from market edge (why any particular trade has a positive expected value). Finally, any mention of promotional bonuses demands extra scrutiny. Across the industry, bonus schemes frequently come with turnover clauses that impede withdrawals—accepting such incentives can complicate settlement later.

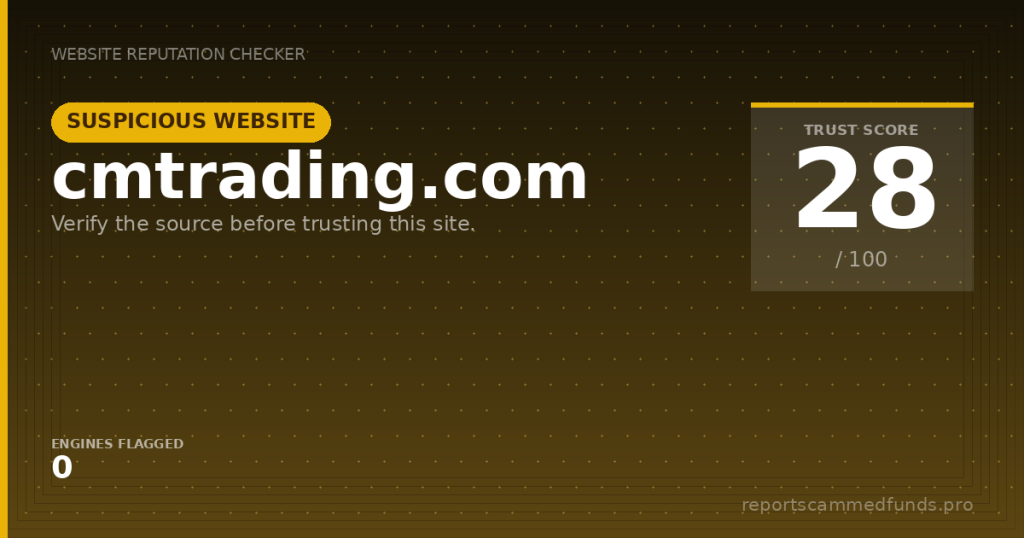

License & regulatory status

The brand publicly states that it is supervised by the Financial Sector Conduct Authority (FSCA) in South Africa. FSCA registration, if valid and applicable to the trading entity that holds client money, provides a degree of oversight, including basic conduct standards and supervision of financial service providers. However, South African regulation is not equivalent to a tier‑1 framework like the United Kingdom’s Financial Conduct Authority (FCA) or Australia’s ASIC. Critically, South Africa does not operate a standing retail compensation scheme akin to the UK’s FSCS, which means clients may have less recourse if the firm fails.

Prospective clients in the UK, EU, Australia, or North America should be aware that we did not find evidence of the brand holding local authorizations in those jurisdictions. Without passporting or local licensing, protections like FCA’s conduct rules, AFCA’s dispute resolution in Australia, or ESMA’s rigor on leverage may not apply to your account. Put simply: if you are outside South Africa and open an account, you are likely contracting with a South African entity under South African law. That leaves you to rely on the FSCA framework and your own cross‑border legal options rather than the stronger tools available under local tier‑1 regimes.

We searched accessible regulator sources for explicit warnings or enforcement actions naming cmtrading.com and did not locate a current, formal notice by major European regulators at the time of this review. This is not a clean bill of health; it simply means no active public censure surfaced in our checks. Warnings often lag behind consumer harm, and names can change or operate via affiliated entities. Readers should verify the precise legal name disclosed on the website against the FSCA’s register and ensure the authorization covers the activities being offered to them.

Some marketing claims—such as segregated client funds, negative balance protection, and robust best‑execution policies—are encouraging if true, yet these require careful verification. We recommend reading the Client Agreement, Order Execution Policy, and Risk Disclosure in full, and then confirming the firm’s legal entity, trading name, and approval status on the FSCA database. If the site claims affiliations or oversight by non‑South‑African bodies (FCA, ASIC, BaFin, CySEC, CFTC), request a direct link to the regulator page and verify independently. Any resistance to providing straightforward documentary proof of licensure is a major warning sign.

User feedback

Public commentary about CMTrading is mixed, which is not unusual for leveraged CFD brands but still demands attention. On the positive side, some users appreciate the educational resources and hand‑holding from assigned account managers or coaches. A subset of reviews describe successful small withdrawals and courteous support via chat or phone, especially among South African clients who use local banking rails. However, the reliability of positive testimonials on broker‑adjacent forums is hard to validate, as brokers sometimes run incentives that nudge satisfied clients to post reviews after smooth onboarding experiences.

The most serious complaints concentrate on withdrawals and post‑profit treatment. Traders report that after initial wins or when requesting larger‑than‑usual withdrawals, the process slows dramatically with repeat document requests, unexplained ‘compliance reviews,’ or demands to close open positions and wait through additional settlement cycles. Others point to bonus terms and turnover requirements that they say were not adequately highlighted at the time of deposit, effectively freezing a portion of their balance. We also note references to ‘surprise KYC’ hurdles that appear only after funding, not before, which is a classic pattern in the high‑risk retail trading space.

Another recurring theme is pressure from ‘account managers’ to increase deposits or adopt riskier tactics—such as copying aggressive traders or trading around news—sometimes framed as coaching toward VIP tier eligibility. While managed guidance can be genuine, it can also blur into salesmanship that is misaligned with the client’s risk tolerance. Reports of slippage, spread widening, or platform hiccups during volatile periods are common across the CFD industry and are not unique to CMTrading, but they matter when combined with high‑leverage products. When account‑manager‑influenced decisions lead to losses, clients frequently feel misled even if the fine print defines the broker relationship as ‘execution‑only.’

To be fair, some clients counter that their experiences have been smooth and that delays occurred only when compliance rules legitimately required more verification, especially for cross‑border withdrawals. That said, the pattern of friction after profits and the opacity of bonus‑related restrictions are red flags that should not be ignored. We advise treating all sales or coaching communications as marketing rather than advice and insisting on documented, written explanations for any withdrawal delay. If a withdrawal cannot be processed within the time frames promised in the broker’s own policies, escalate formally and set clear deadlines.

Deposits & withdrawals

Funding appears to include bank cards and international wire transfer, with the likelihood of South African EFT options for domestic clients. Some third‑party payment processors or e‑wallets may be supported, though we could not independently verify which ones are active at present. Across the industry, crypto deposits are increasingly offered by offshore brokers but can sit outside normal chargeback frameworks; we do not recommend sending cryptocurrency to any broker unless you fully understand the loss of recourse. Regardless of method, know that proper Know‑Your‑Customer (KYC) and anti‑money‑laundering checks are mandatory and should be completed before you risk significant funds.

Withdrawal friction is the flashpoint in many user narratives. Delays commonly stem from incomplete KYC files, mismatches between deposit and withdrawal methods, or outstanding bonus turnover clauses. Less acceptably, some clients describe serial document re‑requests, video verification calls, and shifting justifications that extend timelines beyond what is advertised. Fees, currency conversion spreads, and correspondent bank charges add to the pain, particularly for cross‑border wires. When withdrawals take longer than promised, brokers often blame banks; yet consistently missed timelines are a reliability issue for the broker, not just their vendors.

Practical defenses exist. Decline promotional bonuses to avoid entanglement with turnover conditions, and request in writing that no bonuses be applied to your account. Start with the minimum viable deposit, place a few small trades if needed to satisfy method‑matching rules, and then test a partial withdrawal early. Retain every email, chat transcript, and statement export, and confirm the exact withdrawal processing time frames in the broker’s legal documents rather than relying on sales promises. Should friction arise, escalate in writing, reference the broker’s own policies, and set a strict deadline before moving to formal complaints and chargebacks.

Why unregulated brokers are risky

FSCA authorization, if valid for the entity handling client funds, is better than no oversight. However, it is not on par with tier‑1 jurisdictions like the UK (FCA), Australia (ASIC), or the United States (CFTC/NFA). South Africa does not provide an automatic retail compensation scheme, so if a dispute turns into insolvency or a refusal to pay, clients may be left pursuing civil claims with limited practical recovery. For overseas clients, cross‑border enforcement can be slow and expensive, especially when contracts specify South African law and venue.

CFDs themselves are structurally high risk due to leverage and overnight charges. Many retail clients lose money when volatility spikes and spreads widen, particularly around economic news or thin‑liquidity periods. Copy trading and social trading can compound the problem by piggybacking on the track records of unknown traders whose risk management can change without notice. Where marketing controls are lighter than in tier‑1 regimes, the temptation to over‑promise educational ‘edges’ or VIP privileges can push customers into positions they do not fully understand.

If you reside outside South Africa, you should expect weaker domestic recourse. Regulators like the FCA, BaFin, CONSOB, and ASIC regularly publish warnings against unlicensed cross‑border solicitation, particularly for high‑leverage CFDs and crypto‑derivatives. Even if no warning names this brand today, the absence of local authorization means you are unlikely to benefit from your home regulator’s dispute schemes. For that reason, some readers may prefer a broker with firm, verifiable licensing in their own jurisdiction, even if spreads are slightly higher, because recourse and compensation can matter more than headline pricing.

How to get help if you’ve been scammed

If you have already deposited and are facing withdrawal delays or suspect misconduct, act fast. Contact your card issuer or bank immediately to initiate a dispute or chargeback, citing the timeline promised by the broker and any unmet obligations. Ask your bank to block further charges and cancel any continuous payment authorities connected to the account. Preserve all records: deposit receipts, chat logs, emails, account statements, and screenshots of the broker’s policies and time frames as they appeared when you signed up.

Next, report the case to the relevant authorities. South African clients can lodge complaints with the FSCA, attaching documentary evidence and a clear chronology of events. UK readers should file with Action Fraud; US readers with the FTC and the FBI’s IC3; EU readers with their national regulator and consumer protection agency. Keep your narrative factual and organized—regulators respond better to well‑documented timelines than to generalized allegations. Simultaneously, notify the broker in writing that you have opened formal complaints and set a final deadline for resolution.

For specialized guidance, our team can help you structure your evidence and plan next steps. Visit reportscammedfunds.pro to request case assistance, including dispute strategy, liaison with payment providers, and advisories to avoid common traps. We never ask for upfront ‘recovery fees’; beware of recovery scam outfits that cold‑call victims after public reports. Use only the contact details published on reportscammedfunds.pro and do not share remote access or additional IDs with any third party claiming they can ‘unlock’ your funds. Early, informed action significantly raises your odds of a successful outcome.

Conclusion

CMTrading is not a fly‑by‑night operation; it appears to have been active for years and presents itself under South African oversight. These are positive signals. Still, recurring themes in user feedback—withdrawal friction, sales pressure, and opaque bonus terms—keep this broker in our caution zone. For some readers, the combination of non‑tier‑1 oversight and mixed complaints will be reason enough to look for alternatives with stronger regulatory protection.

If you decide to proceed anyway, tighten your defenses. Verify the exact legal entity and authorization on the FSCA register; decline all bonuses; start with the minimum; and test withdrawals early before increasing exposure. Keep every interaction in writing and avoid allowing anyone to ‘manage’ your account or conduct trades on your behalf. A competent broker will be transparent about fees, timelines, and restrictions and will not balk at documenting them.

Our overall view: CMTrading merits cautious scrutiny rather than a blanket green light. The burden of proof is on the broker to demonstrate reliable execution and frictionless withdrawals under consistent, verifiable rules. Until that proof is clear and sustained, treat every promise through the lens of risk management. Your capital is safer where regulatory protection and company behavior converge in the customer’s favor.