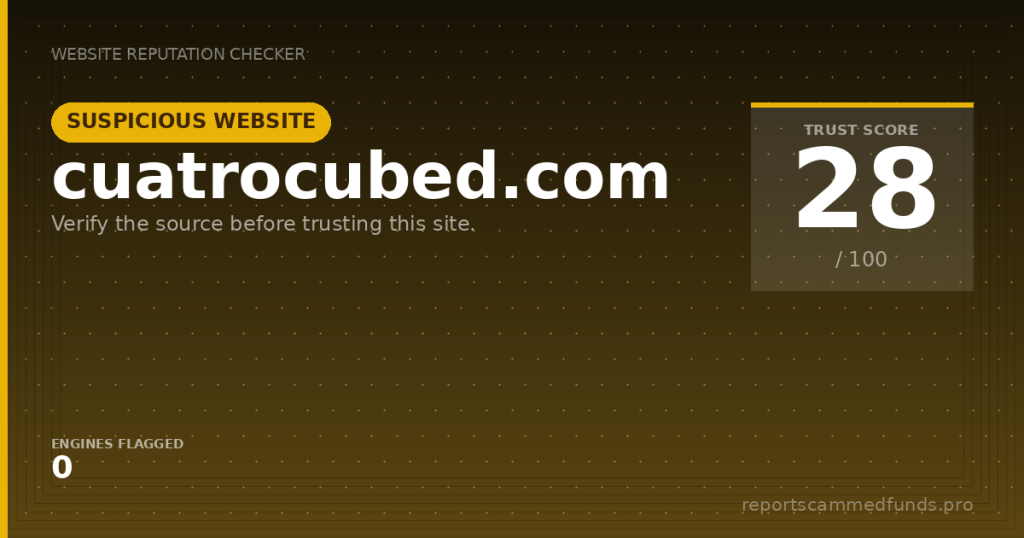

Trading platform & site functionality

We attempted to assess cuatrocubed.com’s functionality and purpose, but the site did not load during our checks. Without access to the live pages, we cannot confirm whether the brand is pitching investment products, software services, consulting, or something else entirely. This absence of basic visibility is notable in itself: credible businesses typically ensure consistent uptime, transparent navigation, and clear explanations of what they do. Even a minimalist one-page site commonly lists a mission statement, a product summary, and a way to reach support.

When evaluating an unknown domain, we look for fundamentals such as an About page naming the operator, a Contact page with verifiable details, and legal pages (Terms of Service, Privacy Policy, and if relevant, Risk Disclosure). We also check for transparent pricing, support hours, and any third-party certifications that can be independently tested. None of these were observable here due to the site’s unavailability. If the platform were meant to facilitate transactions or account creation, downtime and missing disclosures would present both operational and trust concerns.

If cuatrocubed.com is in any way a trading or investment venue, we would expect to see mention of the platform type (for instance, MT4, MT5, or a proprietary web interface), supported instruments, spreads, fee structures, and onboarding steps including KYC. Without those details—or any evidence of a functioning onboarding flow—users are left guessing at the nature of the service. It’s also standard for financial platforms to provide demo environments or walkthroughs and to publish help-center articles. The absence of these indicators, visible or cached, leaves a gap that risk-conscious users should treat conservatively.

Beyond content, there are basic technical and user-experience cues that help set expectations: a valid TLS certificate presented consistently, a cookie consent banner (where required), social media links that lead to active, branded accounts, and a status page or support notice explaining downtime. It is possible the operator is rebuilding or migrating, but if so, a placeholder notice is typically published to reassure users. In the absence of such messaging, it becomes difficult to distinguish a temporary outage from a chronically dormant or abandoned web property. That ambiguity is itself a material risk for anyone contemplating a transaction or account-based relationship with the brand.

License & regulatory status

Licensing and regulatory oversight matter most when a website facilitates trading, investment, or other financial intermediation. If cuatrocubed.com is targeting retail clients with financial products, it would generally require authorization from the appropriate watchdog in each market it serves—such as the FCA in the UK, BaFin in Germany, ASIC in Australia, or the CFTC/NFA in the United States. We found no on-page evidence of any such approvals, nor any license numbers we could verify. Absent clear disclosures, it is prudent to assume the site is not authorized for regulated financial activities until proven otherwise.

It is also common for questionable operators to imply legitimacy by referencing corporate registrations in offshore jurisdictions or by displaying regulator logos without providing verifiable license identifiers. Users should be cautious of phrases like “regulated under international law” or vague claims of compliance that cannot be cross-checked on official registers. Properly regulated firms name the entity that holds authorization, the jurisdiction, and the specific license number, and those details can be found in the regulator’s public database. Any claim lacking this traceability should be treated skeptically.

If, on the other hand, cuatrocubed.com is a non-financial business—say, a software studio or advisory—formal financial regulation may not apply. Even in that scenario, reputable companies publish essential elements: the legal entity behind the brand, a real-world office location or registered agent, and clear customer-service channels. They also provide service agreements and privacy notices that meet jurisdictional standards, as well as information on dispute resolution. The inability to confirm these basics significantly undermines the site’s credibility, regardless of industry.

For cross-border solicitations, the burden on the operator is even higher. A firm marketing to EU residents needs to consider ESMA rules; marketing to UK clients triggers FCA requirements; and U.S. outreach for derivatives or leveraged trading invokes CFTC/NFA rules and potentially SEC oversight if securities are involved. Claims such as “registered in St. Vincent” or “licensed by a business authority” do not grant permission to promote or deliver regulated services in those key markets. Users should verify any jurisdictional permissions on the official regulator websites before committing funds, and treat a lack of disclosures as a significant red flag.

User feedback

Part of our due diligence is to locate independent user feedback across mainstream forums, social platforms, and consumer-complaint boards. For cuatrocubed.com, we did not find a critical mass of credible, detailed user reports that would help to establish a track record—good or bad. While the absence of complaints might appear positive at first glance, in practice it often reflects low visibility, newness, or inactivity rather than trustworthy performance. In other words, a thin public footprint does not equate to safety.

In cases where unknown sites have later proven problematic, recurring themes appear in the complaints: withdrawal blockages after initial profits, sudden demands for “tax” or “commission” pre-payments before releasing funds, or surprise KYC hurdles only after a user requests a payout. Some users report being steered to third-party messaging apps (WhatsApp, Telegram) where high-pressure tactics are applied and promises are made that are absent from the nominal website. Others cite managed-account pitches that result in rapid, unexplained losses, followed by silence from the operator. We are not asserting these patterns apply to cuatrocubed.com, only that these are high-frequency scenarios in adjacent cases.

We also look for corporate transparency signals in social media footprints: a staffed LinkedIn page listing the team, a Twitter or Facebook account posting timely service updates, and clear escalation channels for support. When those channels exist and show consistent activity over time, the chance of long-running deception is generally lower. In the absence of verifiable corporate social profiles—or if profiles exist but are skeletal and rarely updated—users should proceed cautiously and demand written terms before engaging.

Finally, context matters: newly registered domains that solicit funds without providing a physical address, audited financials (where relevant), or third-party attestations tend to be poor bets. Even when an operator is simply early-stage, it is still best practice to offer transparency about the team, the legal structure, and the security of client data and money. Without that, consumers risk entering a one-way relationship where the operator controls the flow of information and the customer has limited leverage if disputes arise. That imbalance is at the heart of many online frauds, and it is why modest skepticism is justified here.

Deposits & withdrawals

Because the site was not accessible during our visit, we could not confirm any accepted payment methods or payout processes for cuatrocubed.com. If the operator requests deposits, you should expect clear terms up front: supported methods (cards, bank wires, e-wallets), fee schedules, minimum and maximum transaction amounts, and processing timelines. It is also normal to see the name of the beneficiary entity for bank transfers and the card descriptor users will recognize on their statements. A lack of payment transparency is a hallmark of risky operators because it obscures who is actually receiving funds and how disputes are handled.

If cryptocurrency is the only accepted deposit option, that is a critical red flag in a retail context. Crypto transfers are effectively irreversible, making them attractive to bad actors who want to avoid chargebacks and clawbacks. Another warning sign is pressure to deposit via gift cards or obscure payment gateways without buyer protection. Reputable businesses that serve a broad consumer base typically support standard, regulated payment channels and provide receipts that identify the merchant of record.

Withdrawal policies deserve equally careful scrutiny. Patterns we see in problematic cases include unexpected identity-verification demands triggered only after a withdrawal is requested, claims that the account must achieve a certain “turnover” before funds can be released, or demands to pre-pay a large “tax” or “commission” to unlock the balance. None of these conditions should be accepted without a signed, dated agreement reviewed before depositing. A legitimate operation publishes its withdrawal timelines, lists all fees, and explains exactly how to escalate a stuck payout.

If the site ultimately proves to be non-financial but requires account registration, consider what data you are handing over and how you would request deletion. Proper operators detail data-retention, account-closure, and erasure rights in their privacy policies, and they provide a dedicated email or ticketing system for such requests. When these channels do not exist—or when the company identity is unclear—recovering your data or obtaining a verifiable response can be difficult. This is another reason to delay account creation until transparency improves.

Why unregulated brokers are risky

Engaging with an unverified or unregulated online service carries multiple risks, the most immediate being a lack of recourse if money or data go missing. Without oversight from a recognized authority, there is no investor-compensation scheme and no supervisor to compel fair dealing. Disputes become private matters where the operator may simply stop responding. In that environment, even good-faith issues—like a technical outage—can create disproportionate harm for users.

Data and identity risk should not be underestimated either. Many scams hinge on collecting copies of passports, driver’s licenses, and proof-of-address documents under the guise of KYC, only to weaponize that data later. It can be used to open accounts elsewhere or to launch targeted phishing attacks. If a website cannot clearly explain why it needs sensitive data and how it will be protected, it is safer to refrain from sharing it.

Jurisdictional ambiguity compounds these problems. Some operators pick offshore or minimal-oversight jurisdictions and then add terms mandating arbitration in venues that are expensive or impractical for customers. Others rely on multi-entity structures to create confusion about which company is responsible for service delivery. Consumers should insist on clarity: who the counterparty is, where it is registered, and which courts or regulators can be approached if something goes wrong.

Finally, transient online operations can disappear as quickly as they appear. It is common to see domain hopping—shuttering one website and opening another under a new name—once complaints accumulate. That churn makes reputational due diligence more challenging, and it is why stability, corporate identity, and verifiable licensing matter. Until cuatrocubed.com demonstrates those attributes, the prudent stance is to stay on the sidelines.

How to get help if you’ve been scammed

If you have already sent money or shared sensitive information in connection with cuatrocubed.com, act quickly. First, stop all communication with the operator and document everything: emails, chat logs, transaction receipts, and any names used by representatives. If you paid by card or bank transfer, contact your issuing bank immediately and request a chargeback or recall, describing the situation as a potential fraud or misrepresentation. The faster you move, the better your odds of interrupting or reversing a payment flow.

For cryptocurrency transfers, notify the exchange or wallet provider you used, provide the transaction hash, and ask whether they can mark the receiving address as suspicious or freeze onward transfers if funds remain on-platform. Parallel to that, file reports with your local law-enforcement body and fraud agency: in the UK, use Action Fraud; in the U.S., report to the FBI’s IC3; in the EU, contact your national police or consumer-protection authority. Reporting creates official records that banks and platforms consider when reviewing dispute claims.

Preserve your device security. If you installed any remote-desktop tools at someone’s request or shared passwords, revoke access, change credentials, and run a reputable security scan. Monitor your credit reports and consider placing a fraud alert if you shared ID documents. Be alert for follow-on contact from “recovery agents” demanding upfront fees; these are often recovery scams that compound losses under the promise of getting your money back.

For guided assistance, you can reach our team at reportscammedfunds.pro. We review documentation, help structure bank and platform submissions, and coordinate regulator reporting where appropriate. While no recovery path is guaranteed, a coherent case file and prompt action significantly improve outcomes. Submit a case at reportscammedfunds.pro and we will advise next steps based on your jurisdiction, payment method, and evidence.

Conclusion

On balance, cuatrocubed.com presents more questions than answers. The site’s inaccessibility during our review, the absence of visible corporate disclosures, and the lack of an established public track record collectively point to elevated risk. That does not prove malicious intent, but it does remove the key ingredients—transparency, accountability, and verifiable licensing—that earn user trust. In this state, a cautious reader is justified in withholding engagement.

If the operator is legitimate and undergoing maintenance or a relaunch, it should publish a dated status notice, provide alternative contact methods, and prominently display its legal entity, address, and terms. If it offers financial services, it should list regulator authorizations with identifiers that can be confirmed on official registers such as the FCA, BaFin, ASIC, or the CFTC/NFA. Restoring confidence is not complicated; it simply requires the same disclosures responsible businesses make every day.

Until those signals appear, we recommend avoiding deposits, refraining from account creation, and not sharing identity documents. If you encounter direct outreach tied to this domain—especially pressure to move conversations to private messaging apps, or requests for crypto-only payments—treat it as a high-risk scenario. Save copies of all communications and do not agree to pay additional “release” or “tax” fees to unlock funds; that is a common escalation tactic in fraud cases.

Should the site come back online with clearer information, revisit your assessment with due diligence: confirm the company in official registries, validate any regulatory claims, and test support responsiveness with non-sensitive inquiries. Until then, the safest course is to step back. Your vigilance—combined with verification using primary sources—remains the best defense against online loss.