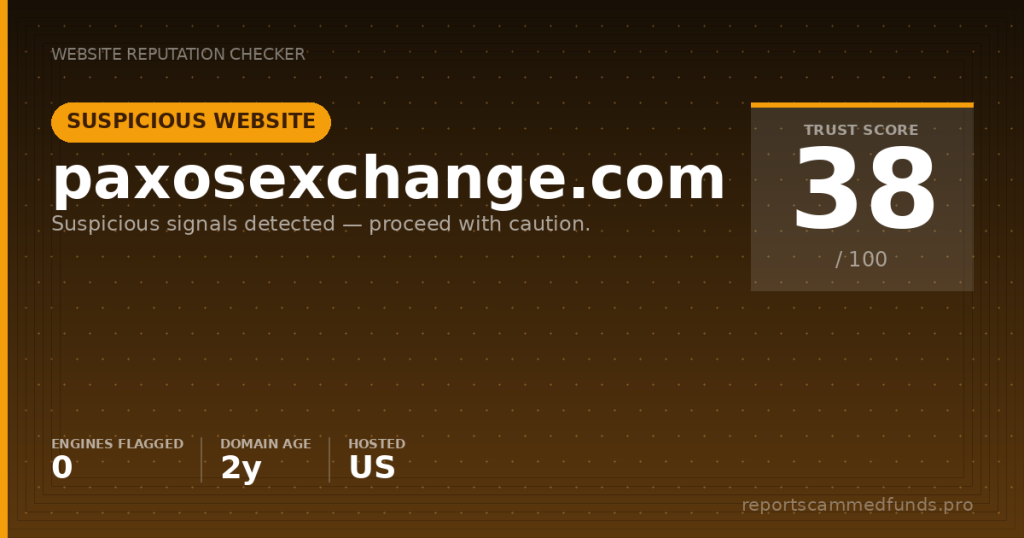

Trading platform & site functionality

Paxosexchange.com loads as a modern, single-page web application over HTTPS, fronted by a CDN. The landing page markets an “online trading platform” with promises of strong Web3 security and a global client base. Visuals include market-themed imagery and a charting widget style that resembles public chart providers. The copy suggests cryptocurrency access and a premium, institutional feel, but concrete details about instrument lists, commissions, or spreads are thin on the ground. Instead of exhaustive product documentation, the site leans on marketing slogans that sidestep the operational realities a genuine broker would spell out.

Under the hood, the app uses WebSocket-style live connections and calls to an external API endpoint at webapi.chan178pro.com for core data. That pattern is common in white‑label trading shells, where a front-end is skinned with a brand while the critical pricing, symbol lists, or even account functions are piped through a separate service. If you’re a retail client, this means your experience depends not only on the site operator but also on a third-party backend you have not vetted. Such dependencies can complicate support, dispute resolution, and technical accountability when things go wrong.

We saw references and outbound links to an array of major financial names and crypto businesses—household institutions and well-known exchanges—and a common market charting provider link pattern. However, mere links or mentions are not evidence of partnership or custodial arrangements. A regulated, enterprise-grade platform would typically publish formal partnership statements, custody chains, audit reports, or at the very least clear terms with named counterparties. Without those, consumers are left to trust a high-gloss interface that has not established the basics: who holds client money, who routes orders, and under what legal framework.

Finally, the user journey is heavily marketing-led. There is no straightforward, public set of disclosures about leverage, margining logic, local-law onboarding restrictions, or conflict-of-interest mitigation (for instance, dealing-desk models or whether the operator acts as principal). Retail traders evaluating fees, slippage protections, and withdrawal processes are unlikely to find the evidence they need to make an informed decision. That absence of specifics is not a minor quibble—it is precisely where many retail losses and disputes later originate.

License & regulatory status

A trading service aimed at the public—in particular one that implies derivatives or CFDs—ought to state its regulation plainly: a license number, the registered entity name, and the supervisory authority (for example, FCA in the UK, CySEC in the EU, ASIC in Australia, BaFin in Germany, or NFA/CFTC in the US). On paxosexchange.com, none of those anchor points are disclosed or independently verifiable. We found no license numbers, no filings, and no audited financial statements tied to a traceable legal entity. That is a sharp departure from how authorized firms present themselves and a primary reason why this site warrants skepticism.

Equally important is the brand proximity to the real, regulated Paxos Trust Company, which operates at a different official domain. Brand-similar names are a classic way to ride on a trusted firm’s reputation without bearing its regulatory obligations. Absent a clear legal statement that explains any relationship (if any) to the well-known firm—and we found no such statement—consumers should assume there is none. Regulators such as the FCA, CONSOB, BaFin, ASIC, and the CFTC routinely warn against name‑cloning and brand passing off; traders who conflate names can end up sending funds to entities outside the supervisory perimeter.

Our checks did not surface a current, formal warning from authorities specifically naming paxosexchange.com at the time of review. That, however, should not be mistaken for a green light. Warnings often trail real-world victimization; in the interim, unlicensed sites can accept deposits for months. The absence of a warning does not equate to safety; what matters is whether the operator is authorized to take your money for the activity it is selling. On that front, paxosexchange.com has not established credentials.

User feedback

Independent, verifiable user feedback about paxosexchange.com is scarce. We could not locate a large body of credible third-party reviews that would let us evaluate the platform’s reliability across deposits, trading, and withdrawals. In many cases, promotional comments dominate early search results for young domains—but these are often seeded by affiliates or the operator itself and should not be treated as objective signals. In the absence of diverse, detailed accounts with transaction evidence, it is prudent to assume that reported experiences are incomplete or optimized for marketing.

Where public complaints surface for similar unregulated platforms, they tend to converge around predictable patterns: withdrawal blockages after profit, sudden demands for surprise “tax” or “unlock” fees, a new Know-Your-Customer (KYC) check triggered only when money is requested back, and managed‑account arrangements that lead to heavy, untraceable losses. We are not asserting that paxosexchange.com has followed those patterns—only that these are the risks most frequently reported by users who later seek help. Without a license, a named legal entity, and clear on-platform terms to counter those risks, prospective clients are left with very little protection if disputes arise.

If you have direct, documented experiences—good or bad—related to paxosexchange.com, maintain all communications, transaction records, wallet hashes (for crypto transfers), bank confirmations, and screenshots. Such artifacts are crucial if you later need to dispute a charge, file a police report, or seek case assistance. Absent that trail, it becomes much harder to prove misrepresentation, unfulfilled withdrawal promises, or unauthorized trading.

Deposits & withdrawals

The platform does not make a transparent, up‑front disclosure of accepted deposit methods, fee schedules, or withdrawal processing timelines on the public pages we reviewed. For unregulated crypto-heavy sites, it is common to see crypto wallet deposits emphasized because they are fast and, critically for the operator, hard to reverse. Card and bank‑wire funding may also be offered, but the decisive test is always the exit: how quickly and under what conditions will funds be released when you ask to withdraw?

On high‑risk sites, withdrawal friction often appears only after a user is in profit or requests a full balance return. Typical roadblocks include requests for additional KYC after deposit, demands for upfront “tax” or “liquidity” payments to “unlock” funds, unexplained anti‑money laundering (AML) holds, or fees that must be paid from outside the platform rather than deducted from the balance—an especially telling red flag. Any platform seeking extra payments before allowing a withdrawal is signaling misalignment with standard, regulated practice.

If you are considering funding an account at paxosexchange.com, do not rely on chat assurances. Insist on written, platform‑hosted terms covering: withdrawal time frames; fees; limits; reversal rights; treatment of chargebacks; and dispute handling procedures naming the responsible legal entity. If such terms are missing or vague, treat that as a primary reason to avoid sending money.

Why unregulated brokers are risky

Trading through an unregulated platform exposes you to hazards no risk disclosure can neutralize. There is no prudential oversight, no capital adequacy checks, and no supervisory testing of client‑fund protections. If the operator commingles client assets or routes orders internally as principal, you may face conflicts of interest without even knowing it. In the event of insolvency or fraud, there is often no investor compensation scheme to fall back on.

Jurisdictional challenges compound the problem. Many lightly documented platforms structure themselves through layers of shell entities or operate entirely without a published company address. That setup frustrates chargebacks, civil claims, and law‑enforcement service of process. Even when you can identify an entity, cross‑border enforcement is slow and expensive—practical barriers that bad actors count on to discourage recovery efforts.

The absence of a supervisor also erodes basic consumer expectations. Regulated brokers are accountable for complaint handling, publication of key information documents, segregation of client money, market abuse monitoring, and adherence to conduct rules. Unregulated sites shoulder none of those obligations unless they choose to, which means the client carries nearly all of the downside if anything goes wrong. That is why regulation is not a formality; it is the line between promises and enforceable duties.

How to get help if you’ve been scammed

If you have already deposited money with paxosexchange.com and are facing resistance on withdrawals or suspect misrepresentation, act quickly. First, contact your bank or card issuer. Explain the situation plainly and ask about a chargeback or recall; emphasize any misleading claims, lack of licensing, or withdrawal obstructions, and provide copies of terms (or note their absence) plus all correspondence and transaction records. Time matters: card schemes have strict windows for dispute filing.

For crypto transfers, assemble the full on‑chain trail—transaction hashes, wallet addresses, and timestamps—and file a report with your local cybercrime office. In the United States, submit at ic3.gov; in the United Kingdom, use actionfraud.police.uk; in the EU, consult your national police cyber portal. Simultaneously, report the platform to your financial regulator (e.g., FCA, BaFin, ASIC, CONSOB, AMF) so they can assess and, where appropriate, issue public warnings that may help others avoid losses.

You do not have to navigate this alone. Our publication operates a reporting and case-assistance channel at reportscammedfunds.pro. Share a concise timeline, proof of payments, screenshots of the platform, and copies of all operator communications. We can help you map recovery options, prepare better-structured bank or card disputes, and connect you to specialized counsel where warranted. Early, well‑documented action materially improves your chances of a positive outcome.

Conclusion

Paxosexchange.com presents polished marketing and a functioning web app, but the essentials are missing: a named, verifiable operator; provable regulation; and detailed, on‑platform terms covering fees, withdrawals, and client‑fund protections. The domain’s brand proximity to a known regulated firm without a declared relationship adds further risk of consumer confusion. In our view, those are not minor gaps—they are decisive risk indicators.

Could this be a new, legitimate venture in the process of maturing into full transparency and compliance? Perhaps—but responsible firms do not accept retail money first and assemble the trust framework later. They publish licenses, legal entities, and complete terms before inviting deposits. Until paxosexchange.com meets that baseline, treating it as a safe place for your funds would be an act of faith, not due diligence.

Our recommendation is straightforward: avoid depositing funds or sharing sensitive documents with paxosexchange.com. If you are determined to proceed, limit exposure to money you can afford to lose, test withdrawals early and often, and document every step. Better yet, select a broker or exchange with clear licensing, named ownership, and an established track record.