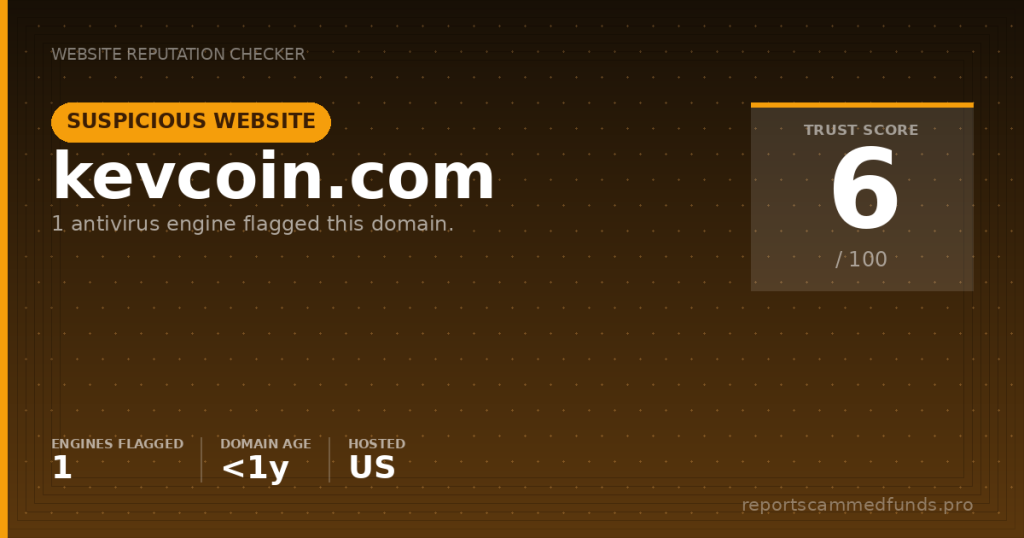

Trading platform & site functionality

Kevcoin.com loads as a single‑page web application with a markets view, a signup/login flow, and a dashboard-style interface. The front end is delivered through bundled JavaScript and CSS, and the site makes API calls to load configuration, currency lists, and a basic news module. Google reCAPTCHA is present on the authentication flow, and the site instruments performance via a client-side analytics beacon. The platform is accessible across several language paths, implying a global pitch rather than a region-specific launch.

From a user’s vantage point, the functionality emulates a typical centralized exchange landing page: lists of coins, percentage changes, and prompts to create an account. What’s missing is just as important as what is shown. We did not see clearly presented fee schedules, order types, custody arrangements, or a description of how client assets are handled and segregated. Nor were independent audits, SOC reports, or wallet transparency disclosures anywhere obvious; that omission matters for any entity that could be entrusted with customer crypto or fiat.

The UX borrows familiar design cues—popular card network logos, promotional imagery, and multi-lingual toggles—to convey maturity. However, the connective tissue that seasoned users expect in a real exchange environment is thin: no apparent legal entity name in the footer, no registered office address, and no obvious links to compliance documentation like risk disclosures, AML/KYC policy details, or conflict of interest statements. While some content may appear after account creation, the lack of pre‑registration transparency is itself a warning sign.

On the engineering side, the use of a content delivery network and modern TLS is standard and not inherently problematic. The site appears to be responsive and fast, with a configurable locale that adjusts parts of the interface. That said, a refined shell doesn’t substitute for robust, verifiable substance. Exchanges must be held to a higher bar because they handle client assets and sensitive data. Without demonstrable proof of licensing, bank rails, custodian arrangements, and a named operator, the platform’s utility—no matter how polished—should be treated as unproven.

License & regulatory status

Regulatory posture is the decisive factor for any platform that touches client money. In the United Kingdom, crypto asset businesses need to be registered with the Financial Conduct Authority (FCA) for AML supervision. In the European Union, the MiCA framework increases transparency and oversight obligations. In the United States, exchanges often fall under multiple layers: federal AML registration (FinCEN as a Money Services Business) and state-level money transmitter licensing. Other major jurisdictions—Germany’s BaFin, Australia’s ASIC, Italy’s CONSOB, and Singapore’s MAS—maintain their own registries.

We examined Kevcoin.com’s public-facing materials for licensing claims, registration numbers, or links to regulator entries and found none. We also could not independently verify a Kevcoin entity in major public registers like the FCA, BaFin, ASIC, or MAS registers, nor could we locate credible references to a FinCEN MSB listing. That does not rule out the existence of some corporate structure behind the site, but a legitimate exchange advertising “global” service should be able to point to at least one provable license or registration.

This absence of verifiable authorization is compounded by the domain’s infancy. Reputable exchanges typically highlight oversight with direct register links and clear corporate identities—complete with company numbers, local addresses, and named directors—because regulators require and customers expect it. When a site encourages deposits but stays silent on who runs it and under what law, users lose the protection that a named regulator would otherwise provide.

We also note that no regulator warnings specific to Kevcoin.com were found in our scan window; however, that should not be mistaken for approval. New domains often fly under the radar in their first weeks and months. The correct inference is not that the site is cleared—it is that it has not been scrutinized or sanctioned yet. Until proper licensing is shown and verifiable, the platform must be treated as unregulated and high-risk.

User feedback

Because the domain is extremely new, there is little to no credible user feedback available in mainstream forums, consumer sites, or developer communities. That vacuum does not clear the platform; it simply reflects that it hasn’t built a public track record. In our experience, rushed promotions sometimes seed testimonials or recycled screenshots that cannot be independently verified. We advise readers to treat any early “success stories” or guaranteed‑profit narratives as inherently suspect unless they can be tied to real, longstanding accounts with corroboration.

In the broader crypto arena, red flags often start appearing in patterns: withdrawal blockages after profits are realized, sudden “surprise KYC” requests only after deposit and trading, changes to bonus terms that make withdrawals impossible, or customer support that turns unresponsive once larger sums are at stake. We do not ascribe these behaviors to Kevcoin.com specifically because we cannot test all flows live with funds, but these are the markers that experienced users watch for when a platform lacks regulatory cover and an established reputation.

If new experiences begin to surface, they will likely revolve around deposit friction, unclear fee deductions, and delayed withdrawals subject to opaque compliance reviews. Keep detailed records—timestamps, transaction IDs, screenshots, and correspondence—if you proceed against our recommendation. In the early lifecycle of a platform, contemporaneous evidence can make the difference in recovering funds via chargeback or helping regulators shut down bad practices more quickly.

Deposits & withdrawals

The site’s interface and imagery suggest support for mainstream card brands and crypto transfers, but we could not confirm the actual deposit methods without opening and funding an account. Displaying logos for Visa or Mastercard does not prove an active acquiring relationship or confirmed acceptance; it only shows a design choice. Legitimate exchanges ordinarily publish a precise list of payment rails, settlement timelines, fees, and territorial limitations—before you register—because these are core to user decision-making.

In withdrawal contexts, the industry’s most common pain points are opaque pending queues, repetitive KYC checks after funds are profitable, and unilateral re-interpretation of bonus or volume rules that trap balances. Absent a verifiable license, users have limited recourse when the platform becomes arbitrarily slow or imposes terms that were not disclosed clearly upfront. We saw no clear, pre‑registration documentation of withdrawal timeframes, fee tables, or the identity of banking partners and custodians, which would normally anchor user expectations.

Before sending any money, insist on written confirmation of deposit and withdrawal methods, the exact schedule of fees (network, spread, maker/taker, and withdrawal), and what documents are required to release funds. If answers are vague or you are pushed to “just try a small deposit,” step back. With crypto and cards, the avenue for reversing a transaction can be limited or time‑sensitive, and platforms can exploit ambiguity by offering contradictory guidance later.

Why unregulated brokers are risky

Entrusting assets to an unregulated platform is not just a reputational risk—it is a structural one. Without a supervisor like the FCA, BaFin, ASIC, CONSOB, MAS, or a comparable authority, there is no standardized complaints pathway, no imposed capital buffers, no client-money segregation rules, and no external audit obligations that can be enforced. If the operator mishandles funds or refuses withdrawals, you are relying purely on their goodwill, not the threat of regulatory penalty.

Crypto markets are volatile and increasingly targeted by boiler‑room operations and “advance-fee” ruses. Scenarios range from account managers who pressure users into topping up for “unlock fees,” to platforms that simulate profits in a dashboard but block all redemptions until additional taxes are paid via the platform. Those classic fraud markers are harder to sustain under regulated scrutiny because the operator could lose a license and face public enforcement, but in an unregulated setup the deterrents are weaker.

Even if the operator’s intentions are benign, the lack of a regulator leaves users exposed to operational collapse—whether from mismanagement, security breaches, or frozen banking relationships. When no one has verified the company’s solvency, custody solutions, or liquidity providers, users shoulder the full downside of a failure. That’s why robust exchanges showcase independent oversight and third‑party attestations; without them, the promise of yield or fast execution is just that—a promise.

How to get help if you’ve been scammed

If you have already deposited funds and are encountering delays, first contact your card issuer or bank immediately to ask about chargeback or dispute options. Provide evidence such as screenshots, emails, chat logs, and any on-site messages indicating withdrawal blockages or changing terms. Act quickly—chargeback windows and dispute rights are often time‑limited, and a fast, well-documented filing improves your odds.

Next, report the incident to your national authority. In the UK, file with Action Fraud and note any transfers or card charges; in the US, submit a complaint to the FTC and IC3; in the EU, contact your national financial regulator and local law enforcement; in Australia, reach out to ASIC’s reporting channels. These reports help investigators identify common operators, freeze suspicious accounts, and issue public warnings that can prevent additional victims.

Finally, you can request specialized assistance. Our team at reportscammedfunds.pro reviews cases involving high‑risk brokers, exchanges, and recovery‑scam spin‑offs, and can advise on documenting losses, preserving digital evidence, and coordinating parallel reports to banks and regulators. Be wary of anyone promising guaranteed recovery for an upfront fee—those are often “recovery scams.” Seek advice before paying any third party and use only traceable, regulated payment methods.

Conclusion

Kevcoin.com is presenting the aesthetics of a global crypto exchange without the disclosures that responsible operators put front and center. The domain is days old, we found no verifiable licensing, and at least one security source already marks the site as high risk. In a sector where trust hinges on oversight and transparency, those are deal‑breakers.

Our position is straightforward: do not deposit funds or share personal documents until and unless the operator publishes a verifiable license and a legal entity that can be checked in an authoritative register. Even then, read terms closely, confirm fees in writing, and test withdrawals with a tiny amount before scaling. The opportunity cost of waiting is trivial next to the potential loss from a blocked withdrawal or vanishing balance.

If you have been approached by someone urging you to fund a Kevcoin.com account, step back and verify every claim independently. High‑pressure timelines, promised returns, or insistence on crypto-only deposits are red flags. Safety first: treat this site as unproven and proceed, if at all, only after hard evidence of regulation and a strong, third‑party audit trail are available.