Trading platform & site functionality

Facebook is a large-scale social networking platform that provides user profiles, friend connections, pages, groups, marketplace listings, events, advertising tools, and a private messaging layer that typically routes to Messenger. The site automatically redirects from the bare apex to www.facebook.com with a consistent 301, and it serves modern web assets from its own content delivery domains such as static.xx.fbcdn.net. In ordinary use, visitors encounter login and sign-up interfaces, localized language options, and footer links to policy pages and related Meta properties. The platform is designed for high availability and fast load times, leaning on its global edge infrastructure, and it generally renders quickly on broadband and mobile networks alike.

From a technical security perspective, the site enforces HTTPS with a certificate issued by a mainstream public CA, supports HTTP/3 over QUIC, and advertises strict transport security. Its certificate’s subject alternative names cover related hostnames used for static assets and messaging, and certificate-transparency compliance is evident. CAA records indicate a controlled issuance pathway, which is a best practice to limit unexpected certificate minting. The front-end code also includes a well-known developer-console warning that discourages users from pasting unknown scripts—an anti–self-XSS measure that reputable platforms use to reduce account takeovers caused by social-engineering tricks.

Facebook’s functional surface is vast, but on-page behaviors are coherent and typical of a mature, mass-market application. Cookies are set for session handling, security, and personalization, and the privacy and cookies pages explain how these elements work at a high level. Cross-links to Instagram, Messenger, and Meta’s product pages are presented through tracked outbound redirects, which is consistent with large platforms’ attribution and safety layering. We observed no broken flows, unusual payment prompts, or exotic plug-ins on the public landing page; the platform’s performance and reliability signals align with what users expect from one of the most visited websites in the world.

License & regulatory status

There is no indication that facebook.com holds or claims a financial-services authorization such as an FCA, BaFin, ASIC, CONSOB, CFTC, or FINMA license—nor would it be expected to, because Facebook is not an investment broker or trading venue. The site functions as a social network and advertising platform, which falls outside the scopes of market-intermediary regulation. Accordingly, the absence of a broker license is not a red flag here; it is simply not the relevant category.

Where regulation does come into play is data protection and consumer law. Facebook, through its operator Meta Platforms, is subject to a patchwork of privacy and consumer-protection regimes (for example, GDPR in the EU or state privacy laws in the U.S.), and the company publishes policy and help-center pages that explain account control, data access, and reporting features. Those frameworks are not the same as prudential financial regulation, but they do define obligations in areas like consent, transparency, and redress routes for privacy complaints.

Some financial-adjacent functions—such as ad billing, fan subscriptions, or charitable donation tools—are facilitated within the Facebook environment. Those rely on payments processing arrangements and country-specific compliance handled by Meta entities or partners, and terms for such features are documented in platform policies. We did not observe the site representing that it holds an investment, derivatives, or e-money license directly on the public landing page, and no official regulator warnings targeting facebook.com as a fraudulent financial operator were found in the automated scan.

User feedback

Public commentary about Facebook is vast and mixed, reflecting the platform’s scale and role in online life. Typical positive themes include the ease of reconnecting with friends, the reach achievable through pages and groups, and the maturity of the ad system’s targeting and analytics. On the other side, long-standing critiques include moderation disputes, uneven support responsiveness for account issues, and frustration with changes to the news feed and reach. None of those themes by themselves imply the domain is unsafe; rather, they are the experience contours of a ubiquitous social platform.

A recurring pain point reported across forums involves account access and recovery after phishing, malware, or weak-password incidents. Because Facebook accounts can be monetized through ads or impersonation, criminals target them aggressively. Users who fall for “support” impersonations or paste malicious code into the developer console can lose access until recovery measures are completed, and that recovery can feel slow or confusing. The platform’s self-XSS warning is designed to reduce one common path to compromise, but personal hygiene (unique passwords, 2FA) remains critical.

Advertisers sometimes raise billing or policy-enforcement complaints, particularly when an automated review flags a creative or a business page. These disputes usually route through help-center tickets, appeal workflows, or Business Support channels and can take several back-and-forth rounds. While such issues can be costly for small firms if ads halt during reviews, they are not intrinsically evidence of a scam by facebook.com. They are the operational realities of scaled, rules-driven systems handling billions of impressions across jurisdictions and risk thresholds.

Deposits & withdrawals

Facebook is not a brokerage and does not solicit deposits or trading balances on its main consumer interface. However, some features do involve payments—ad accounts, page boosts, fan support, event tickets, or in-app purchases like Stars—depending on country and eligibility. Accepted methods commonly include credit and debit cards and, in some markets, PayPal or other processors, though exact options vary by region and business verification status and are not independently verified here.

For those who transact on the platform (for example, advertisers), the billing setup occurs in Business or Ads Manager under documented terms. Chargebacks and disputes follow the rules of your card issuer or payment provider, and the platform provides receipts and statements that can support reconciliation. As with any online payment, monitoring transactions and setting spend limits is advisable, especially for pages with multiple admins or agencies involved in campaign management.

If a user sends money externally because of a pitch encountered on Facebook—say, someone met through Messenger who requests crypto, gift cards, or wire transfers—that transaction does not involve facebook.com’s own checkout and offers no platform-provided buyer protection. In such cases, your recourse is primarily through your bank or card provider. That distinction matters: the site itself is safe to visit, but fraudsters may attempt to lure payments off-platform, where recovery becomes more difficult.

Why unregulated brokers are risky

Because Facebook is not a regulated investment intermediary, it should never be relied on as a channel to transfer funds to strangers for trading or guaranteed returns. Boiler-room operators, romance scammers (so-called pig-butchering), and fake recovery agents often begin contact through social media profiles or groups and then push victims to off-platform apps or wallets. None of that misuse changes the legitimacy of facebook.com itself, but it does shape the risk environment in which you interact.

Impersonation is another real hazard. Criminals clone official pages, lift logos, and buy cheap ads pointing to counterfeit sites that closely mimic reputable brands. Users who do not inspect URLs carefully, or who accept unsolicited investment invitations, can be diverted to phishing portals and coerced into advance-fee payments. The safest course is to navigate to known good domains directly, verify blue-check verifications where available, and avoid clicking links in messages from unknown senders.

When considering any financial proposition encountered on Facebook—managed accounts, crypto mining packages, forex signals, or recovery services—assume it is unregulated unless you can independently confirm a license with the named regulator (FCA, BaFin, ASIC, CFTC, or your local authority). Refuse pressure to act fast, decline screen-sharing requests, and never send identity documents to strangers. The platform offers reporting tools; use them when you see impersonation or fraud patterns so the content can be reviewed and, where appropriate, removed.

How to get help if you’ve been scammed

If you have already lost money after contact initiated via Facebook, act quickly. Contact your bank or card issuer to request a chargeback or recall; provide all receipts, chat transcripts, and URLs. If you sent a wire or crypto, notify your bank immediately and file formal complaints—time is critical, but even late reports create records that help wider investigations.

Report the incident to the appropriate authority where you live. In the United States, submit to the FBI’s IC3 and the FTC; in the United Kingdom, use Action Fraud; in the EU, contact your national police cybercrime unit or consumer-protection agency. Use Facebook’s on-platform reporting tools to flag the user, page, or ad so that trust and safety teams can review and, if applicable, take enforcement action against the content and associated accounts.

For tailored case guidance, you can contact our team at reportscammedfunds.pro. We help readers document evidence, map payment paths, and coordinate outreach to banks, processors, and the correct regulators. While no service can guarantee fund recovery—especially with crypto or cross-border transfers—early, organized action steeply improves your prospects and helps prevent further harm to others.

Conclusion

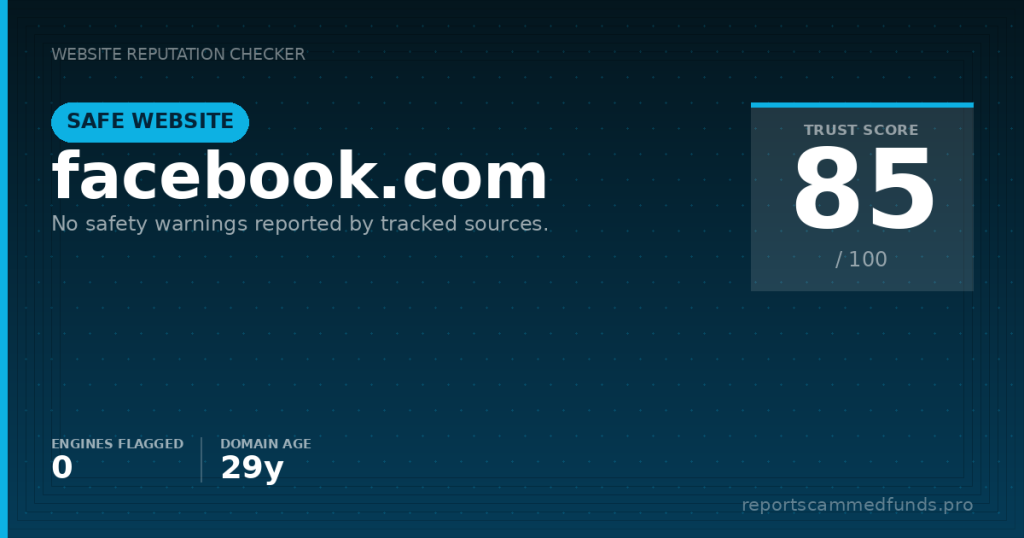

On balance, facebook.com itself presents as a legitimate, mature, and well-defended domain operated by a globally recognized company. Automated scans show clean results, the certificate chain and security headers are in order, and the site’s behavior matches what we expect from a high-traffic platform. Nothing in our review suggests the domain is a scam.

That does not mean everything encountered via Facebook is trustworthy. Social networks are a favored hunting ground for fraudsters who impersonate brands, romance-investment coaches, or tech support. Treat offers with caution, verify identities independently, and keep your account locked down with strong authentication and up-to-date recovery options.

If you arrived at this review because something about a Facebook interaction felt off, follow the help steps above and err on the side of caution. The website is safe to use, but your safety still depends on careful judgment about who you engage with and where you send money. When in doubt, slow down, verify, and seek advice.